Beginning with the tax year 2020, the IRS issued a separate information return form to report nonemployee compensation (NEC) payments to independent contractors. Form 1099-MISC for miscellaneous income was redesigned, and NEC-related payments from Box 7 of Form 1099-MISC moved to a new Form 1099-NEC. In January 2022, these 1099 forms were revised again.

Recipients use Form 1099-NEC and Form 1099-MISC to file their federal and any applicable state tax returns.

Form 1099-NEC doesn’t entirely replace Form 1099-MISC for payers needing to report other miscellaneous types of payments besides nonemployee compensation.

What is Form 1099-NEC?

Form 1099-NEC is a new IRS information return tax form for reporting at least $600 in nonemployee compensation payments and tax withholding in the course of a trade or business per calendar year. Reportable payments are to business owners or independent contractors that don’t file their federal income tax returns as a C Corporation or S Corporation.

Form 1099-NEC is also used for reporting payer direct sales of $5,000 or more in consumer products to the recipient for resale.

Payments made to an individual, partnership, estate, or sometimes a corporation may be reported on Form 1099-NEC. Despite the general exception for corporation payees, reporting attorneys’ fees (Box 1, Form 1099-NEC) or gross income (Box 10, Form 1099-MISC) of corporations providing legal services is required on a Form 1099).

Independent contractors, whose income payments may be reported by payers on Form 1099-NEC, include:

- freelancers

- self-employed service providers operating as individuals or small businesses, including:

- attorneys,

- CPAs,

- tax professionals, and

- real estate agents not paid as employees, using Form W-2.

Independent contractors and other suppliers provide a Form W-9 with their contact information and taxpayer identification number (TIN) to their clients or customers for filing forms 1099-NEC to report nonemployee compensation and backup withholding and 1099-MISC to report miscellaneous types of payments. Payers send (or efile) a copy of Form 1099-NEC to the IRS, applicable states, and payees.

Types of taxpayer identification numbers include SSN (social security number), ITIN (individual taxpayer identification number), ATIN (taxpayer identification number for pending U.S. adoptions), or EIN (employer identification number).

The payer needs to follow the IRS backup withholding rules for nonemployee compensation by withholding income taxes if a payee didn’t provide them with a taxpayer ID number (TIN) or the IRS lets the payer know that the taxpayer identification number for the payee is incorrect.

Instead of filing Form 1099-NEC for nonemployee independent contractors that are nonresident aliens, use Form 1042-S for reporting contractor payments and IRS Form 1042.

What is Form 1099-MISC?

Form 1099-MISC is an IRS form used by payers to report specified miscellaneous income payments, generally over $600, made in the course of a trade or business during a calendar year.

More specifically, payers should file Form 1099-MISC to report:

- $10 or more in royalties (Box 2) or broker payments in lieu of dividends or tax-exempt interest (Box 8)

- $600 or more in:

- Prizes and awards, other income payments, and cash paid from a notional principal contract to an individual, partnership, or estate, in general (Box 3);

- Fishing boat proceeds (Box 5)

- Medical and health care payments (Box 6)

- Crop insurance proceeds (Box 9)

- Payments to an attorney (Box 10) – claims gross income

- Section 409A deferrals (Box 12)

- Nonqualified deferred compensation (Box 14)

How can your business report supplier payments correctly?

Download our “Executive Summary: KPMG on AP Tax Compliance” to learn about global supplier tax compliance.

Use AP automation software for self-service supplier onboarding and verification, and payment tracking to efficiently prepare 1099 forms to report global supplier payments.

What is the Difference Between Form 1099-NEC and Form 1099-MISC?

The difference between IRS Form 1099-NEC and Form 1099-MISC information returns is that Form 1099-NEC is used by payers to report nonemployee compensation and follow backup withholding rules. Form 1099-MISC is used by payers to report information on other types of miscellaneous nonemployee payments.

The IRS provides instructions for tax Form 1099-NEC and Form 1099-MISC with more details about each form and the differences. Read other Tipalti articles covering Form 1099-NEC and Form 1099-MISC for more information, including differences in filing Form 1099-NEC vs Form 1099-MISC.

Which Items Changed on Form 1099-MISC?

With the January 2022 revision, the 1099-MISC form doesn’t include a form year but allows payers to indicate the calendar year for which payments are being reported in this 1099 information return.

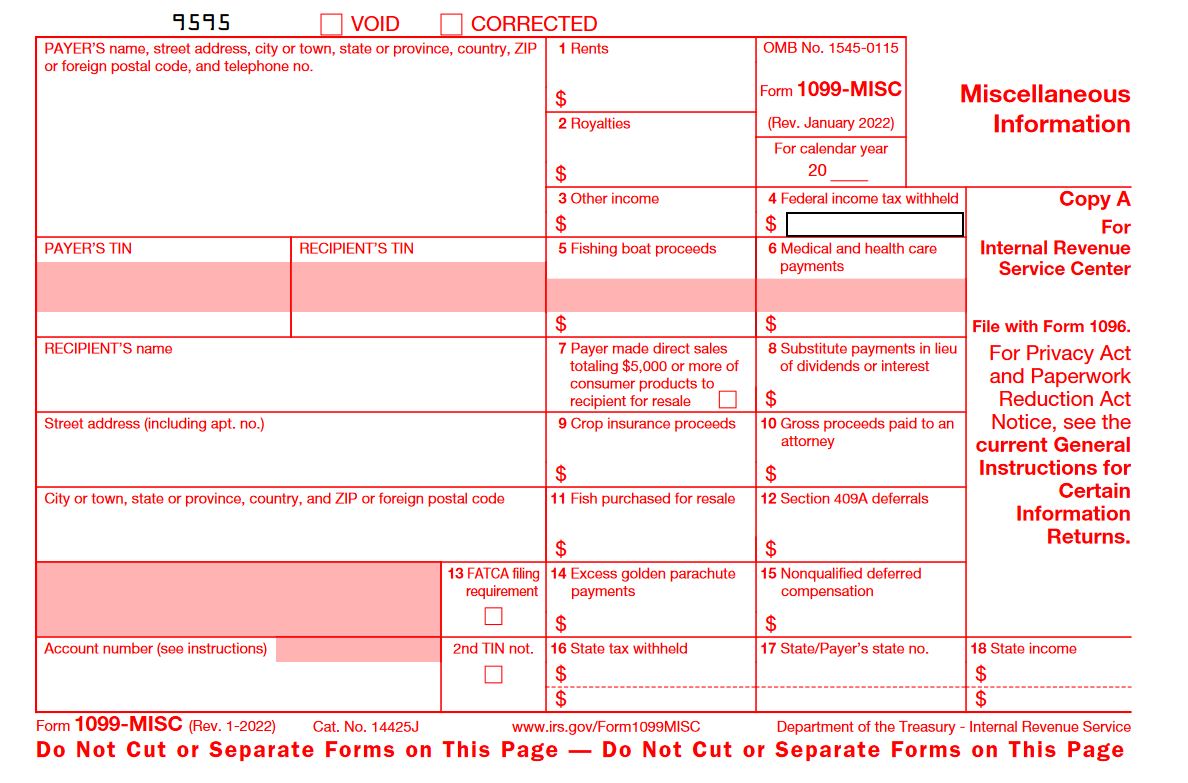

A sample of Form 1099-MISC that shouldn’t be copied and filed with the IRS is shown above. The following items or boxes changed in Form 1099-MISC, beginning with tax year 2020.

Box 7, Form 1099-MISC Changes

Box 7 of Form 1099-MISC for reporting nonemployee compensation was removed from the tax form. Instead, Form 1099-NEC is used to report nonemployee compensation, beginning for the tax year 2020. Instead, Box 7 of Form 1099-MISC is a checkbox for payer made direct sales of $5,000 or more.

Box 9, Form 1099-MISC Change

Report crop insurance proceeds in Box 9 of Form 1099-MISC.

Box 10, Form 1099-MISC Change

Report the gross proceeds to an attorney in Box 10 of Form 1099-MISC, even if the attorney files a corporation return. The gross proceeds are for claims paid to an attorney without deducting attorney’s fees (which would be reported on Form 1099-NEC, Box 1).

Box 12, Form 1099-MISC Change

Report Section 409a deferrals in Box 12 of Form 1099-MISC.

Box 13, Form 1099-MISC Change

If applicable, check the FATCA filing requirement checkbox in Box 13.

Box 14, Form 1099-MISC Change

Use Box 14 of 1099-MISC to report excess golden parachute payments.

Box 15, Form 1099-MISC Change

Use Box 15 of 1099-MISC to report nonqualified deferred compensation income.

Boxes 16, 17 & 18, Form 1099-MISC Changes for State Information

Payer filers use these Form 1099-MISC boxes to report state filing information to each applicable state tax department and recipient needing the information to file a state tax return.

Box 16 – state taxes withheld

Box 17 – state identification number

Box 18 – amount of income earned in the state

The U.S. has nine states with no income taxes:

- Alaska

- Florida

- Nevada

- New Hampshire (only investment earnings)

- South Dakota

- Tennessee

- Texas

- Washington

- Wyoming

Which Items Changed on Form 1099-NEC?

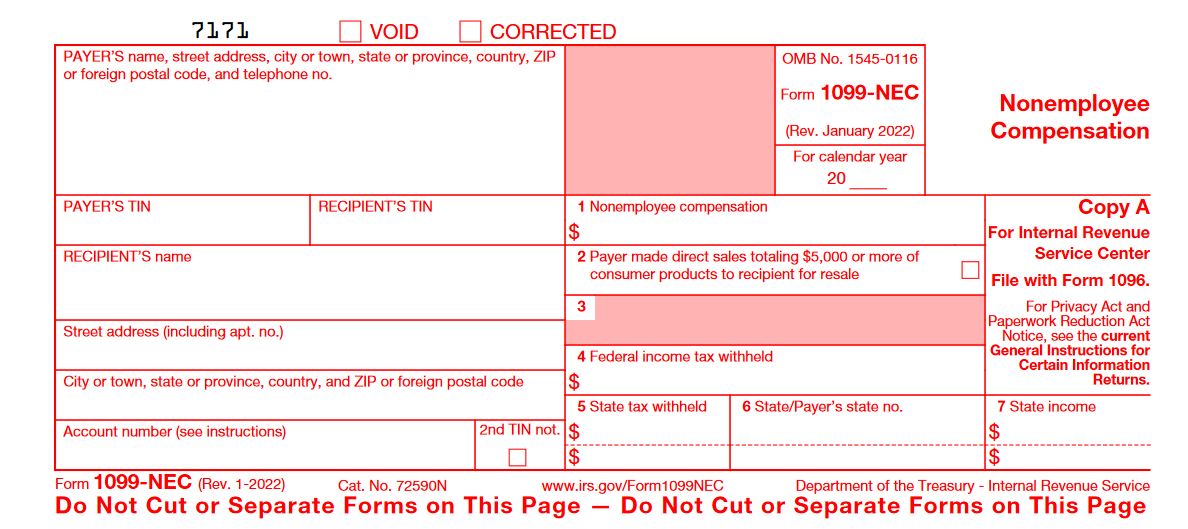

A sample of Form 1099-NEC that shouldn’t be copied and filed with the IRS is shown above.

With the January 2022 revision, the 1099-NEC form doesn’t include a form year but allows payers to indicate the calendar year for which payments are being reported in this 1099 information return.

Items reported in Form 1099-NEC include:

• A checkbox for VOID or CORRECTED Form 1099-NEC

• Payer’s and Recipient’s contact information and taxpayer identification number (TIN)

• Account number for payee

• Checkbox for 2nd TIN notice

• Box 1 – Total dollar amount of Nonemployee compensation

• Box 2 – Checkbox for Payer made direct sales totaling $5,000 or more of consumer products to recipient for resale

• Box 3 – Currently not used

• Box 4 – Federal income tax withheld in dollars

• Box 5 – State tax withheld in dollars

• Box 6 – State/Payer’s state number

• Box 7 – State income in dollars (paid to recipient)

What is the Due Date for Filing Form 1099-NEC and Form 1099-MISC?

For 2023 due dates covering 2022 payments, the IRS General Instructions indicate the filing deadline for electronic and paper filers of Form 1099-NEC is January 31, 2023, a month after the end of the tax year for which payments are being reported, with no 30-day automatic extension offered. Form 1099-NEC is sent to recipients by January 31, 2023.

Although Form 1099-MISC must be sent to the recipient by February 15, 2023 (if amounts are reported in boxes 8 or 10), payer businesses must file Form 1099-MISC with the IRS by February 28, 2023, if paper filing or March 31, 2023, if efiling the form with the IRS. If payees have hardship conditions, they may be able to extend the deadline for filing the 1099 information returns.

The IRS imposes deadlines for filing forms 1099-NEC and 1099-MISC to detect fraud and verify the income of payee recipients when they file a U.S. federal tax return by checking that it includes reportable income from a payer.

How Do You File Form 1099-NEC and Form 1099-MISC?

IRS filing requirements specify that payers should use a separate IRS transmittal Form 1096 for sending each type of 1099 form when filing Forms 1099-NEC and Forms 1099-MISC with the IRS.

When the payer efiles or sends on paper the Forms 1099-NEC and 1099-MISC, Copy A goes to the Internal Revenue Service Center, Copy 1 to the state tax department (if applicable), and Copy B to the recipient.

Conclusion – 1099-NEC vs 1099-MISC and Instructions

IRS Form 1099-NEC for nonemployee compensation and Form 1099-MISC for certain Miscellaneous Information and payments to nonemployees are filed as separate information return forms beginning with the tax year 2020. Form 1099-MISC was redesigned by the IRS when the new Form 1099-NEC was created.

We provided the meaning, usage, difference, and filing deadlines for IRS Form 1099-NEC and Form 1099-MISC information returns. Consult the detailed IRS Instructions for these forms when you prepare them to efile or send as a payer by the deadlines, or receive the forms as a nonemployee payee. To understand global supplier tax compliance with 1099s, get Executive Summary: KPMG on AP Tax Compliance.”