In general, nonresident aliens who receive income in the United States are subject to U.S. federal taxes. This income of non-U.S. citizens can be in the form of earned income or other types of payment. The Internal Revenue Service wants to know about these payments to receive income tax returns from these taxpayers.

It’s important to know what IRS Form 1042-S is and how the process works by reading these FAQs.

What is Form 1042-S?

Form 1042-S is an IRS form titled Foreign Person’s U.S. Source Income Subject to Withholding. Form 1042-S is an information return filed by a withholding agent to report the amounts paid to foreign persons, as described under the “Amounts Subject to NRA Withholding and Reporting.” Form 1042-S applies even if filers didn’t withhold any income tax.

IRS Form 1042-S is a required document for reporting money paid to foreign persons (or those presumed to be foreign) by a U.S.-based business or institution.

Who Uses Form 1042-S?

Non-US citizens or non-US groups, including foreign partnerships, corporations, estates or trusts, use Form 1042-S to report any US-based income they may have received to be accurately taxed on that income, according to US standards. In cases where a tax treaty or other exception to taxation exists, the IRS will still require Form 1042-S to be completed.

What Types of Payments Do You Report on Form 1042-S?

A withholding agent uses Form 1042-S to report U.S. source scholarships and fellowship grants received by foreign students. Form 1042-S also applies to dividends from U.S. companies, deposit account interest, pensions, royalties, real estate income, insurance premiums, compensation from services performed in the U.S., and gambling winnings.

When the 1042-S form is used to report a scholarship or fellowship grant of a foreign national, only the amount over the cost of tuition is reportable.

Real estate income includes REMIC (real estate mortgage investment conduit) for income code 02 excess inclusions of allocated share of taxable income to a foreign partner.

Compensation from services conducted in the U.S. includes:

• Compensation for independent personal services performed in the United States, and

• Compensation for dependent personal services performed in the United States (but only if the beneficial owner is claiming treaty benefits).

In cases where there is more than one type of income, multiple forms must be used. For example, if one person received pension income and royalties, you must use a 1042-S for each.

How is Reporting Income Handled using Form 1042-S?

Under the tax laws of the United States, Form 1042-S is not used to report wages for income tax purposes. Instead, Form W-2 should be used.

However, if earnings are exempt from income tax withholding because of a tax treaty (between the earner’s home country and the United States) that provides treaty benefits, then Form 1042-S can be used. This is to only report wages in excess of the amount that’s exempt from income tax withholding.

Take the treaty between Morocco and the United States. Moroccans who work as independent contractors in the U.S. are exempt from taxation up to $5,000 in total income. This is only under certain guidelines.

For example, if a Moroccan earns $7,250.19 in income, he would receive a W-2 showing $2,250.19 in gross income and a 1042-S reporting $5,000. Although Morocco and the United States have a tax treaty, both IRS forms need to be filed.

What Do You Need to Know about Filing Form 1042-S?

Form 1042-S must be filed with the IRS and a copy should also be sent to the business, student, entity, or employee payee to complete their U.S. federal tax return. It’s the responsibility of the withholding agent to complete the form. The withholding agent could be:

• An employer

• Business

• University

• Other institution

Form 1042-S should be filed regardless of whether tax is withheld or not.

Furthermore, one form must be completed for each tax rate. This is for any given type of income that’s paid to the same earner.

Although Form 1042-S can be filed the old-fashioned way, the IRS does permit electronic filing of the form. The newer electronic method is actually required for withholding agents who have 250 or more forms to submit. Financial institutions are also required to file electronically.

When is IRS Filing on Time for Form 1042-S?

Only one 1042-S should be filed per calendar year. It is due to the IRS and the recipient on March 15th of the year after the relevant payment was made.

If you need more time to file Forms 1042-S, the IRS will grant an extension. To gain more time, you will need to file Form 8809 (Application for Extension of Time to File Information Returns) by the due date of Form 1042-S. Keep in mind that there is no extension for the payment of tax.

Failure to file a 1042-S on time without an extension or not paying any tax due could result in interest and penalties from Uncle Sam.

How are Forms 1042/1042-T vs. 1042-S Used?

The 1042-S form should not be used for income tax purposes. To report income, Form 1042 (Annual Withholding Tax Return for U.S. Source Income of Foreign Persons) should be used. Withholding agents should file 1042 with the IRS instead of with the employee.

If Form 1042-S is filed in hard-copy format, it must be accompanied by Form 1042-T (Annual Summary and Transmittal of Forms 1042-S). One T Form should be used for each type of S form submitted.

Is your business withholding U.S. income tax on foreign supplier payments?

Download our “Executive Summary: KPMG on AP Tax Compliance” to learn about global supplier tax compliance.

Use AP automation software for self-service onboarding of global suppliers, including collecting W-8 or W-9 forms before first payment, supplier name and TIN verification, withholding calculations, and payments tracking for efficiently preparing information returns, including 1042-S and 1099s.

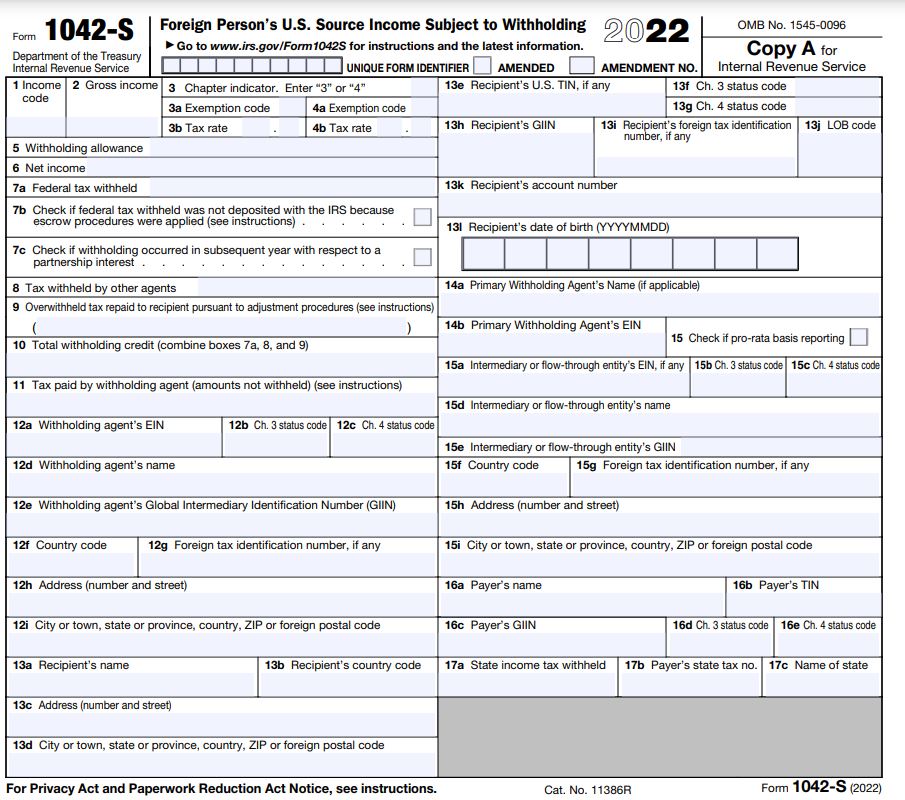

How To Fill Out IRS Form 1042-S

We describe some boxes (line items) in Form 1042-S and provide a screenshot of the IRS 2021 form. Read the IRS Form 1042-S Instructions for more details.

Refer to Instructions for Form 1042-S for a few code changes beginning for 2022, described in the What’s New section.

Box 1 – Income code

Box 1 on Form 1042-S is critical, as this requires the income code that classifies a payment. One form can only have one code. If you’ve received multiple payments from several codes, more than one form must be filed.

Box 2 – Gross income

In Box 2, for gross income (not net income), enter the entire amount paid to the recipient, including tax withholding, for each type of income.

Box 3 – Chapter indicator

Box 3 is the place to enter Chapter 3 or 4. The former is for withholdings that apply to foreign persons, while the latter is for entities that are foreign financial institutions.

Box 3a or Box 4a – Exemption code

Box 3b or Box 4b – Tax rate

If the tax rate entered in Box 3a or 4a is zero, enter an exemption code 01 through 23 from IRS Appendix B of Form 1042-S Instructions in either 3b or 4b, depending on the chapter indicator.

Box 5 – Withholding allowance

Box 5 for withholding allowance applies only to the following Box 1 income codes: 16 for scholarship or fellowship grants, 17 for compensation for independent personal services, 18 for compensation for dependent personal services, 19 for compensation for teaching, 20 for compensation during studying and training, or 42 for earnings as an artist or athlete with no central withholding agreement. Read the Form 1042-S Instructions for special rules applying to a designated withholding agent with a central withholding agreement with the IRS.

Box 10 – Total withholding credit (combine boxes 7a, 8, and 9)

In some situations, a Form 1042-S is filled out just for the records of the recipient. It does not need to be filed with the IRS in this situation. For example, when Box 10 (Withholding Credit) and Box 7a (U.S. Federal Tax Withheld) both show $0, the form does not need to be filed with the IRS. In this situation, Form 1042-S also does not need to be included with the recipient’s tax return.

Box 12f – Country code

Enter the country code of your residence from the IRS list of foreign countries accessible from Form 1042-S Instructions in Box 12f or OC if that country isn’t included in the IRS list.

Box 13f – Ch. 3 status code or Box 13g Ch. 4 status code

In Box 13f or 13g enter the recipient status code from IRS Appendix B to Form 1042-S Instructions.

Box 17a – State income tax withheld

Boxes 17a through 17c relate to any state income tax withheld.

Box 17b – Payer’s state tax no.

In Box 17b, enter the payer’s state tax number.

Box 17c – Name of state

In Box 17c, enter the state name.

In Conclusion

If you are still unsure about which forms to file, it’s always best to read Form 1042-S Instructions, visit the IRS website at ww.IRS.gov, or contact the IRS directly. Don’t take a guess and make a costly mistake. For more foreign and domestic supplier tax rules, get Executive Summary: KPMG on AP Tax Compliance.”