In 2023 alone, Canadian companies engaged in over $1.5 trillion CAD in international merchandise trade, and a World Bank study showed that the global average cost of a simple $200 remittance is a hefty 6% when using traditional banks.

While not used within Canada, understanding IBANs is essential for Canadian CFOs, controllers, accounts payable managers, finance professionals, and business owners dealing with suppliers, partners, or customers in Europe and many other regions.

This guide will demystify IBANs, addressing common challenges like high fees, unfavourable exchange rates, and complex regulations for Canadian businesses.

What is an International Bank Account Number (IBAN)?

IBAN, or International Bank Account Number, is a code used to make or receive international payments. It’s a standard international numbering system used to identify an overseas bank account and is used in more than 70 countries worldwide.

Your IBAN code is different from your Canadian transit and account number – it’s solely used to help overseas banks identify your bank account so you can receive or send international payments.

This is key for Canadian companies doing business with partners abroad who are in countries using the IBAN system. For example, a Canadian e-commerce company paying a software developer in France would need the developer’s IBAN.

Your IBAN includes different numeric identifiers, such as a bank account number and country code, that serve to convey your correct bank and bank account to international banks. An IBAN is a type of bank code. Find more information on bank codes here, including the major types you need to know.

Key Takeaways

- IBAN is short for International Bank Account Number and is used to identify an individual bank account in cross-border payments.

- IBAN codes facilitate international money transfers.

- SEPA is a separate and smaller network than IBAN, each serving different countries. While primarily relevant to Europe, SEPA is still important for Canadian businesses with European dealings.

- An IBAN can be located on your bank statement, through online banking, an IBAN calculator, or the IBAN Registry.

- Your online banking portal (through your Canadian financial institution) should show the IBAN information. Major Canadian Banks, such as RBC, TD, Scotiabank, BMO, and CIBC will provide the necessary IBAN details.

- Keep in mind that online calculators can check the format but not definitively confirm an account’s existence or validity.

Dokka Alternative PTR - The SWIFT network standardized the formats for the IBAN system and owns the BIC system.

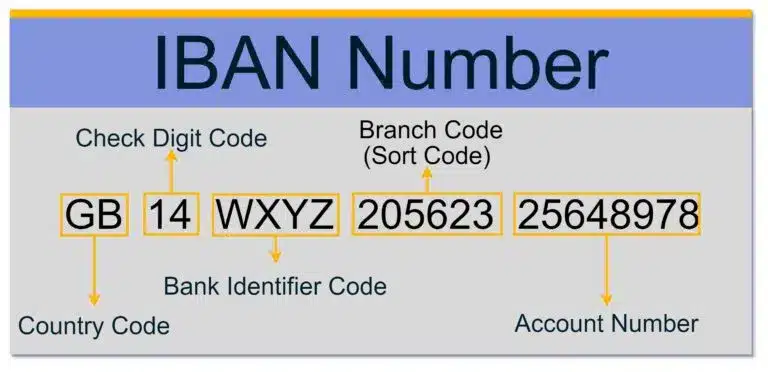

What Does an IBAN Look Like?

In general, an IBAN number is divided into a numbering system comprised of codes (sometimes in the order presented, although it does vary by country):

- Country code (sometimes called location code)

- Check digit code

- Bank identifier code

- Branch code

- Account number

The last three (bank, branch, and account numbers) collectively make up the Basic Bank Account Number (BBAN) and are used to locate a specific bank.

The banking association of each nation decides on the BBAN. The IBAN format is always the same for every country, although the number of digits may vary.

For instance, the United Kingdom uses 22 characters, while France relies on 27. The maximum number that any country can use is 34. Canadian businesses should know that the United States, Australia, and China do not use IBANs.

Please note the IBAN method is mostly used within the majority of European Union countries and other European countries.

This is especially relevant for Canadian companies transacting with Europe since most European nations require IBANs for all incoming and outgoing international money movements.

Always check with your bank if you’re unsure about an international transfer.

Furthermore, the check digit is calculated using a special formula, much like the one used in Canadian banking under CPA 006, and it’s there to make sure everything is accurate.

IBAN vs BIC

A Bank Identifier Code (BIC) is just a general term for a SWIFT code. That’s why the terms are often used interchangeably, like SWIFT/BIC. Technically, the network through which international transfers are sent is the SWIFT network, and the codes are BIC codes.

Whereas an IBAN identifies a bank’s country of business and one’s precise account number within that institution, a BIC (Bank Identifier Code) breaks down into 3 more specific elements to aid a transaction.

It’s composed of alphanumeric characters, namely, a 4-letter bank code, a 2-letter country code, and a branch identifier composed of one letter and one number.

A SWIFT code is similar to a Canadian bank’s institution number, as it identifies the specific bank.

On the other hand, the IBAN is comparable to the combination of the transit number and account number, uniquely pinpointing the specific account for bank account identification.

A BIC is also important to avoid post-transaction costs that can be incurred from fixing a misdirected wire transfer.

IBAN vs SWIFT Code

IBAN and SWIFT codes are both internationally recognized for identifying bank accounts when a transfer is being made. The unique identifier required depends on the country involved and the recipient’s bank.

For Canadian businesses, providing both the IBAN and the SWIFT/BIC accurately is paramount to prevent delays, additional charges, and potential payment setbacks.

It’s worth noting that transactions heading to the United States primarily use SWIFT codes.

SWIFT stands for the Society for Worldwide Interbank Financial Telecommunication. A SWIFT code refers to a specific financial institution in an international transaction, whereas an IBAN number identifies an individual account and the country of business.

It’s the global equivalent of a bank account and a transit number in Canada.

The primary difference between the two codes lies in the information inside.

Learn more about IBAN vs SWIFT codes, including costs, use cases, and examples.

Examples of an IBAN Number

Here are a few examples of IBAN formats from nations with which Canadian businesses often have trade connections:

- United Kingdom: GB29 NWBK 6016 1331 9268 19

- France: FR14 2004 1010 0505 0001 3M02 606

- Germany: DE89 3704 0044 0532 0130 00

- Spain: ES79 2100 0418 4502 0005 1332

How to Find Your IBAN Number

The IBAN is located on every paper bank statement an institution prints. It may also appear inside your web-based account if you use online banking.

Your online banking portal (through your Canadian financial institution) should show the IBAN information if you’re set up to receive international payments. Major Canadian Banks, such as RBC, TD, Scotiabank, BMO, and CIBC, will provide the necessary IBAN details for international money transfers.

If you can’t find it in either of those locations, contact the bank, use the IBAN Registry, or an IBAN calculator tool.

But keep in mind, while these tools can check if the IBAN is in the right format, they can’t guarantee the account actually exists or belongs to the right person.

Does it Cost Money to Use an IBAN?

IBANs are needed for international bank transfers, so expect to pay bank transfer fees. The cost will vary by country and exchange rate, but a processing fee and commission are usually charged.

Canadian banks typically impose fees for international wire transfers, and these can include processing fees, commissions, and potentially exchange rates that aren’t as good as the mid-market rate you might see on financial websites.

It’s a good idea to compare fees and exchange rates from different Canadian banks, and also to explore specialized international payment providers – they might offer better deals.

Main Functions of an IBAN Number

When it comes to international banking, IBANs are a critical piece of information. It serves three main functions for sending and receiving cross-border payments, which are:

1. Allows banks and other financial institutions to quickly note the country of origin for the bank.

2. IBAN pinpoints the exact account number to which the money will be sent.

3. It’s an easy way to double-check the accuracy of a bank’s details and ensure a transfer will be successful.

These three functions are incredibly important for Canadian businesses because accuracy is paramount in making sure that payments are dispatched and received in time.

Which Banks Use IBAN Numbers?

This all depends on where you live. Banks in the United States, Canada, Australia, New Zealand, and China do not use IBAN codes. They use SWIFT codes and routing numbers. IBANs are mostly reserved for European countries.

Canadian banks do not use IBANs for transactions within Canada – instead, they rely on transit numbers and institution numbers. However, Canadian banks will utilize IBANs when sending or receiving international payments to or from countries that mandate them.

For payments within Canada or destined for the US, Canadian businesses will use routing numbers (for the US) or transit numbers (within Canada).

According to the ECBS (European Commerce Banking Services), “generation of the IBAN shall be the exclusive responsibility of the bank/branch servicing the account.”

The Basic Bank Account Number (BBAN) format is decided by the designated payment authority or central bank of each country, and there is no consistency between which formats are adopted.

They may register the BBAN format with SWIFT, but countries are not obliged to do so. The same goes for IBAN numbers. A major difference between the two is that under SWIFT, there is no requirement that BBANs be a certain length.

What is the IBAN Registry?

The IBAN registry is a catalogue of countries that comply with the most recent IBAN standards (ISO 13616). It is published by SWIFT and contains details of each country’s IBAN format.

The registry also provides a history of updates and describes key terms related to IBAN transactions.

Is the IBAN Number Used in the USA?

IBAN numbers are only used in the USA to send money to a foreign bank account that also participates in the International Bank Account Number System.

Currently, US banks do not use the IBAN number domestically. Instead, US banks use ABA routing numbers (for domestic transfers) and SWIFT codes (for international transfers).

Just like in the United States, IBAN numbers aren’t used for transactions within Canada itself.

What Is the Difference Between IBAN and SEPA?

The Single Euro Payment Area (SEPA), as the name suggests, is a payment network in Europe that provides digital transfers within the European Union. This includes places like Spain, Ireland, Hungary, the United Kingdom, and more. It also covers a few countries outside of the union, including Norway, Iceland, Switzerland, and Liechtenstein.

While the European Committee for Banking Standards (ECBS) sets national standards for business identifier codes, the overall SEPA system is also influenced by the policies of the European Central Bank.

In total, the SEPA network works across 28 countries. By comparison, over 60 countries currently use the IBAN system. Multiple currencies can also be sent using IBAN, whereas only Euros can be used on the SEPA network. This is important for Canadian companies to understand, especially if they deal in Europe.

Since its adoption throughout Europe in the late 1990s, some countries in the Middle East and the Caribbean have also begun using the IBAN system for digital money transfers.

Understanding these regulations is crucial, as a majority of Canadian small businesses cite complex regulations as a major challenge in international trade.

Find out more about SEPA payments, including setup, benefits, and requirements.

What is the Purpose of IBAN?

Before International Bank Account Numbers were adopted, different European countries had different bank account number formats, and this discrepancy led to errors in cross-border transactions. International payments would end up in the wrong location, requiring extra fees and time to resolve the issue.

Then, in 1997, the International Organization for Standardization (ISO) proposed a new system of global money movement. Today, this international standard is known as ISO 13616-2:2007.

The result of the IBAN program has been fewer errors in international wire transfers and other financial transactions. Because multiple countries now operate within the same system, it’s also easier for people to send money from one jurisdiction to another.

For Canadian firms, this standardization translates to fewer payment errors, quicker processing times, and lower administrative costs when interacting with international partners who use IBANs.

Despite these advantages, there are issues IBAN cannot address, such as foreign exchange rates.

Navigating the Landscape of International Payments

Successfully managing international payments involves more than just understanding IBANs, SWIFT codes, and BICs. While these are fundamental components, Canadian businesses must also navigate a broader landscape of challenges and opportunities.

This section provides an overview of key considerations, from currency exchange strategies and Canadian reporting requirements to alternative payment methods and maintaining the security and accuracy of your transactions.

Currency Exchange Strategies

Effectively managing currency exchange is a vital aspect of international payments. Here are several tips worth noting:

- Canadian businesses should be aware of the difference between the mid-market rate (the ‘real’ exchange rate) and the rate offered by banks, which often includes a markup.

- Exploring options like forward contracts (locking in an exchange rate for a future date) and currency options (providing the right, but not the obligation, to exchange currency at a specific rate) can help mitigate currency risk.

- Natural hedging, where a company’s revenues and expenses in a foreign currency offset each other, is another strategy to consider.

Canadian Reporting Requirements

Canadian businesses also have to follow reporting rules set by the Canada Revenue Agency (CRA). This includes Form T1134 (Information Return Relating to Controlled and Non-Controlled Foreign Affiliates), which may be needed for businesses with foreign affiliates.

Here are other important Canadian reporting requirements to consider:

- It’s important to understand the definition of a “controlled foreign affiliate” and the specific reporting limits.

- Financial institutions must report large international electronic funds transfers (EFTs) of $10,000 CAD or more to the CRA, and businesses should be aware of this.

- Keeping detailed records of all international transactions is very important for supporting CRA reporting and any potential audits.

Alternatives to Traditional Wire Transfers

Looking to improve efficiencies and save on expenses? Exploring different methods of international payments has a large impact on achieving each.

- International ACH (also known as Global ACH) is a cheaper option than wire transfers, although it may take longer to process.

- Multi-currency accounts let businesses hold and manage funds in different currencies, cutting down on the need for frequent conversions and potentially saving on exchange rate fees.

- While Interac e-Transfer is mainly used for transactions within Canada, some fintech companies are checking out its potential for cross-border payments through partnerships and integrations – a possible future development.

Explore smarter ways to send money abroad

IBANs are just the beginning. Compare global payment methods, understand their costs and use cases, and find out which ones best suit your Canadian business.

IBAN Validation, Security, and the Role of the Registry

Making sure the accuracy and security of international payments is pivotal, and the IBAN system itself plays a key role. We’ve broken down how you can be on the right side through three important, related categories below

IBAN Validation

The check digits within an IBAN allow for bank account validation before a transaction is submitted to confirm the bank account number is correct.

Beyond IBAN-specific check digits, many countries have their own national check digits used within the BBAN. Each country has its own way of determining the algorithm used for assigning and validating these national check digits.

Therefore, when providing an IBAN, you should always communicate in machine-readable form without spaces.

IBAN Security

While it’s completely safe to provide your IBAN (as it only allows others to send money to you), it’s a good idea to stay alert for phishing scams.

Scammers may try to get IBANs and other personal or financial information through misleading tactics.

However, it’s important to remember that the IBAN system itself is meant to cut down on errors and make cross-border payments more reliable.

The IBAN Registry

The IBAN registry, maintained by SWIFT, is a catalogue of countries that follow the latest IBAN standards (ISO 13616, published in 1997 and updated in 2007).

This registry gives details of each country’s IBAN format, updated history, and definitions of key terms.

SWIFT, as the designated Registration Authority, plays a key role in making sure everyone follows the standard.

In the end, the smooth and safe transfer of funds across borders is vital for healthy international markets and trade. IBANs, SWIFT codes, and BICs are all key parts of this process.

The Bottom Line on IBANs for Canadians

IBAN plays an important role in facilitating timely and accurate international payments, especially for Canadian businesses interacting with Europe and other IBAN-using regions.

This guide covered IBAN’s fundamentals – from understanding IBAN structure and validation to differentiating between IBANs, SWIFT/BIC codes, and SEPA. We’ve also explored Canadian-specific details like transit numbers and what the CRA expects you to report, plus ways to handle currency exchange and other payment options.

But knowing all about IBANs is just one step. International payments are still a challenging area with ever-changing rules, fluctuating exchange rates and all sorts of fees.

To succeed globally, Canadian businesses need international payment systems that are streamlined, safe, and don’t break the bank. Download our Comparing Top Global Payment Methods eBook to explore the different approaches of making international payments a source of strength, not a source of stress, for your business.

IBAN FAQs

Do Canadian banks use IBANs?

Canadian banks do not use IBANs for transactions within Canada. However, they use IBANs for international transactions with countries participating in the IBAN system.

What information do I need to provide to receive an international payment in Canada?

To receive an international payment in Canada, you’ll typically need to provide the sender with your SWIFT/BIC code, your bank account number, your bank’s name and address, and potentially your transit number.

Are there alternatives to wire transfers for international payments from Canada?

Yes, there are alternatives to wire transfers, such as international money transfer services. These often have better exchange rates compared to traditional banks.

How do I find my transit number?

Your transit number is a five-digit number that identifies the specific branch of your Canadian financial institution. It’s usually found on your cheques, in your online banking portal, or by contacting your bank.

Is it safe to give out an IBAN number?

It is absolutely safe to give anyone your IBAN number. That’s because it only exposes data that allows someone to send money to you, and not personal account details.

However, be cautious of phishing scams where fraudsters might try to trick you into revealing your IBAN along with other sensitive information.

Is a SWIFT code the same as a routing number?

International organizations use the SWIFT system, whereas routing numbers are only used in the US. In Canada, we use transit numbers for domestic transactions.

Who uses IBAN codes?

As of September 2022, 79 countries are required to use IBAN for domestic and international payments, however, the exact number is difficult to pinpoint and likely higher.

Should I use BIC or IBAN?

If you’re using the IBAN system, you’ll need both. While an IBAN provides data about your individual account, the BIC code is the bank your account is held at.

Can an IBAN be used for direct debits?

An IBAN by itself cannot be used to initiate a direct debit. Direct debits need additional authorization and information beyond the IBAN.

In Canada, pre-authorized debits (PADs) require the account number and transit number, along with a signed agreement. While SEPA Direct Debits in Europe use IBANs, they also require a separate mandate.