In business, cash flow and profit are both critical financial measurements. However, cash flow and profit aren’t the same. Even when a company is profitable, cash flow is an essential concept. If you don’t have enough cash flow to meet the myriad expenses of running a business, it’s almost impossible to maintain financial health over the long term to stay afloat.

For business owners in a small business, understanding the relationship between profit and cash flow helps determine when key decisions need to be made.

Full comprehension of what cash flow and profit mean and how they are optimized in businesses of all sizes is essential for success.

What is Cash Flow?

Cash flow is cash and cash equivalents inflows less outflows. Cash received and spent or invested and debt repayment are categorized as business operating, investing, and financing activities. Cash flow is presented in a U.S. GAAP-required financial statement. Financial management forecasts expected cash flow to meet liquidity needs and obtain financing when required.

Key Takeaways

- Net cash flow is cash (and cash equivalents) inflows less cash outflows.

- Cash equivalents can be readily converted to cash and have an original maturity date of three months or less.

- The cash flow statement, required by U.S. GAAP, includes beginning and ending cash and cash equivalents balances (including restricted cash), sections for operating activities, investing activities, and financing activities, and certain non-cash activity disclosures.

- Free cash flow is operating cash flow minus capital expenditures.

- Discounted cash flow is the present value of estimated future cash flows related to a potential project. DCF is often used to evaluate and compare potential business investments, including M&A, to buy another company.

- Cash flow and profit aren’t the same. Meeting cash flow needs is essential for achieving company success. Inadequate cash flow is the primary reason that many startups and small businesses go out of business.

Types of Cash Flow

Operating Activities Cash Flow

Operating activities cash flow is net cash generated from a company’s normal operating business activities, flowing to net income. In a cash flow statement for a period of time, operating activities are presented either using the indirect or direct method.

The statement of cash flows indirect method, which is more widely used, reconciles net income (loss) from the income statement to cash flow from operating activities. Reconciling items include changes in working capital balances (like accounts receivable, inventory, and accounts payable) and adding back non-cash items ( depreciation and amortization).

In business analysis, working capital is current assets less current liabilities in financial statements prepared using the accrual basis of accounting. Current assets and current liabilities are within one year (short-term) or the length of the business operating cycle.

Investing Activities Cash Flow

Investing activities cash flow is cash inflows for equity and debt investments (in other companies) sold, sale of fixed assets, insurance proceeds for fixed assets, collection of principal on loans issued to borrowers, and cash outflows for acquiring fixed assets, lenders issuing loans to borrowers, and buying other companies through M&A for cash.

Activities related to trading securities (not available for sale or held-to-maturity securities) are considered operating activities rather than investing activities.

Financing Activities Cash Flow

Financing activities cash flow is cash inflow and cash outflow relating to a company’s creditors and business owner or owners. Financing cash flow is the net cash generated to finance an entire company, including equity (treasury stock repurchase and reissuance transactions), short-term or long-term debt, and cash dividend payments.

Cash Flow Formulas

Cash flow formulas include free cash flow, operating cash flow, and discounted cash flow.

Free Cash Flow

Free cash flow is net cash flow from business operations after deducting capital expenditures. Capital expenditures are amounts spent by businesses to buy long-term assets called fixed assets, including equipment, land, and buildings. Free cash flow may be calculated in different ways.

The simplest free cash flow formula is:

Operating Cash Flow – Capital Expenditures

Operating Cash Flow

The formula for operating cash flow (cash flow from operations), which is cash flow from normal business operations, follows. Operating cash flow can be calculated for each accounting period.

Operating Cash Flow = Operating Income + (non-cash) Depreciation and Amortization – Taxes + Change in Working Capital

Discounted Cash Flow

Discounted cash flow (DCF) uses the time value of money to calculate the net present value (NPV) of projected cash flows for a potential investment project. The cash flow analysis justifies its worth, or the business selects a different project for investment when the NPV values are compared.

Discounted Cash Flow = the sum of (Cash Flow for each year ➗ (1+ discount rate for each year))

Discounted cash flow shows years 0 through the number of years of projected cash flows and terminal value of the investment, which is cash generated at the investment project termination date, such as the sale of fixed assets. Year 0 is the year of investment in the project, which often shows negative cash flows.

For example, an investment project or business purchase may be analyzed over 5 years. The time periods for calculating Net Present Value would be years 0-5 plus a terminal value (column shown after year 5).

Businesses may use their percentage Weighted Average Cost of Capital (WACC) to get the discount rate.

You can find the discounted cash flow formula in textbooks or on the Internet and use a table of Present Values to calculate DCF. Zions Bank provides an online Discounted Cash Flow calculator for business valuation. If you prefer, you can use an Excel formula to calculate discounted cash flow.

Operating Cash Flow Ratio

The operating cash flow ratio (also called current liability coverage ratio) calculates the relationship between cash flow from operations and current liabilities which will be paid from cash flow. Companies with a high ratio number (over 1) have financial strength to pay amounts when due.

Cash Flow from Operations ➗ Current Liabiities

Debt Service Coverage Ratio

Debt service = principal + interest payments and recurring contributions to a sinking fund to repay debt. Debt service is calculated for the same time period as net operating Income or EBITDA.

Net Operating Income (or EBITDA) ➗ Total Debt Sevice

Positive or Negative Cash Flow

Positive Cash Flow

Positive cash flow means that the amount of money from cash inflows is greater than cash outflows in a business. Cash inflows minus cash outflows is a positive amount.

Negative Cash Flow

Negative cash flow means that a business has a greater amount of cash outflows than cash inflows. If cash inflows minus cash outflows is a negative amount, the company’s cash flow is negative.

Established fast-growing businesses and startup companies need financing to bridge the gap between the net amount of cash internally generated and their business spending requirements at a point in time to pay suppliers and meet other financial obligations, including investing in M&A transactions to grow.

If you’re looking to improve cash flow and create more liquidity, it requires strategic sourcing. Performing a spend analysis is a good step in understanding why a business has a negative cash flow and what can be done.

Examples of Cash Inflow and Cash Outflow

This section provides examples of cash inflow and outflow.

Cash Inflow

Examples of cash inflow include:

- Borrowed capital like a business loan or line of credit

- Cash sales of products and services

- Money collected from accounts receivable and customer payments

The statement of cash flows shows the different areas in which a business uses or receives cash. It also helps to reconcile the beginning and end of monthly, quarterly, or annual cash balances. If you’re running a cash flow analysis, this is a document you need on hand.

Cash Outflow

- Money spent on paying vendor invoices (accounts payable)

- Payroll

- Taxes

- Rent

- Loan payments

- Other business expenses

For example, if you borrow $50,000 to finance an equipment purchase, the lump sum of capital you receive is considered a “cash inflow,” whereas the payments you make on the loan are considered a “cash outflow.”

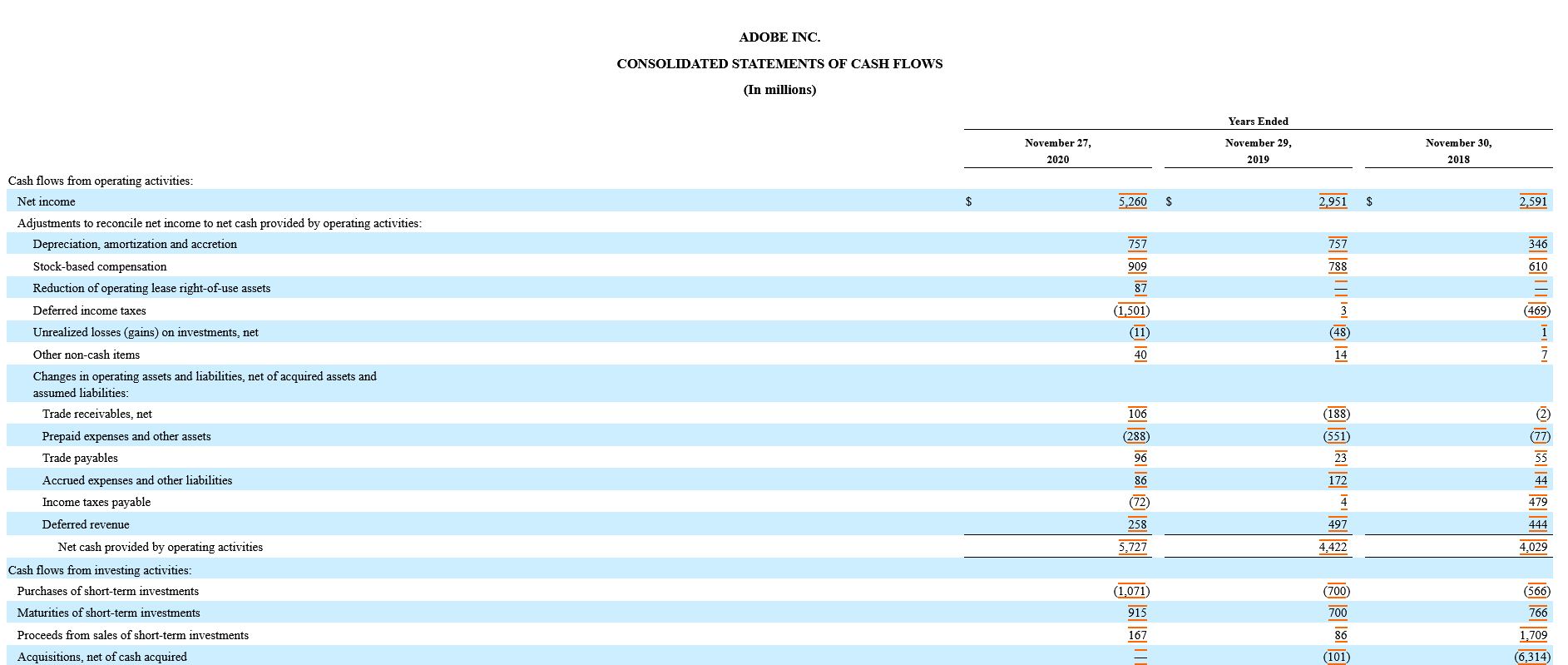

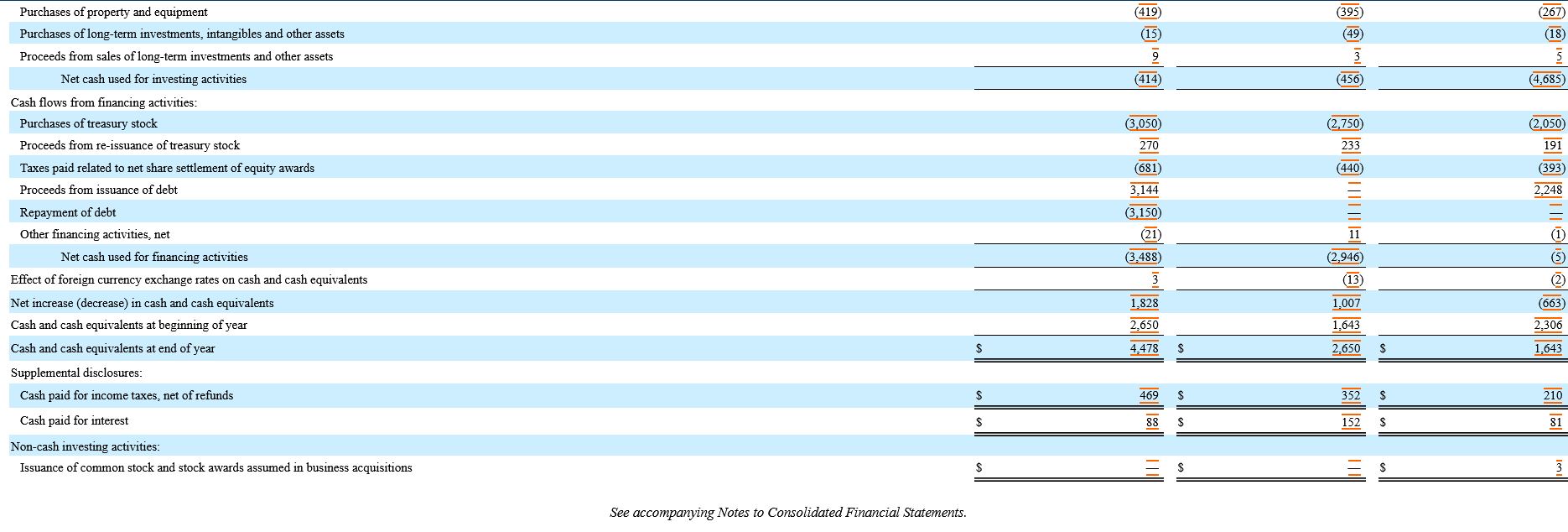

A screenshot from the Consolidated Statements of Cash Flows from Adobe Inc.’s 10-K filing with the SEC for the fiscal year ended November 27, 2020, shows examples of cash inflow and cash outflow line items by category.

Cash Flow Processes

Cash flow processes include cash flow management and cash flow forecasting :

1. Cash Flow Management

Cash flow management is a proactive process for tracking, forecasting cash needs, and ensuring that cash balances will be adequate to pay financial obligations. Cash flow management includes obtaining financing, including tapping a bank line of credit, when needed.

2. Cash Flow Forecasting

Cash flow forecasting projects cash needs and cash balances by time period and includes cash inflow and cash outflow by category.

Cash Flow Statement

The cash flow statement required by U.S. generally accepted accounting principles (GAAP) includes beginning cash and cash equivalents from the balance sheet, three main sections of operating activities, investing activities, and financing activities, ending cash and cash equivalents balance, and non-cash investing & financing disclosure items on the face of this financial statement.

Besides the cash flow statement, other major financial statements are the income statement and balance sheet, which are used to prepare the statement of cash flows.

Cash equivalents, which have an original maturity of three months or less, include money market funds, treasury bills, and commercial paper.

Cash Flow vs Profit

Cash flow is about money “flowing” in and out of your business. What cash is received and what the company is spending in cash is cash flow. The main difference between the two concepts (cash flow vs. profit) is that profit refers to the income statement bottom line, while cash flow refers to the net cash resulting from cash inflows and outflows.

Profit is the amount shown on an income statement after revenue and cost of goods sold are recorded to compute gross profit, operating expenses are deducted, and non-cash expenses are recorded. Both profit before tax and profit after income tax (net income) are displayed on financial statements.

Accounting for profit generally uses accrual accounting rather than cash-basis accounting (sometimes used for income taxes).

Although both concepts are important (cash flow vs. profit), you can’t maintain operational efficiency without adequate cash flow.

Importance of Cash Flow

Cash flow is more important than profit because it keeps the company operating as a going concern.

It’s tough to compare cash flow and profit because it’s apples and oranges. Both systems are important in their own way. While it’s agreed that profitability is desired over time, a business will never get to grow without a solid amount of cash flow. The immediate availability of working capital is what directly affects daily operations.

While profitability provides a snapshot of a financial situation during a specific time period, it doesn’t account for daily processes where net cash flow is critical. Profitable companies fail every year because they have cash flow problems. If a business’s cash is tied up, there’s nothing on hand to cover expenses.

No single metric will satisfy investors and business owners. Both factors must be equally understood to evaluate the financial health of a business. It’s possible for a company to have negative cash flow but still be profitable. It’s also possible for a business to have positive cash flow and good sales, with no profit. Examples include scaling companies and startups.

How to Analyze Cash Flow

Businesses use ratios and cash flow formulas to assess business liquidity and the amount of cash flow available for investments and spending, like free cash flow (shown in the Cash Flow Formulas section).

Conclusion

Your first step to ensuring healthy business growth is understanding cash flow, the difference between cash flow and profit, and the purpose each serves. You’ll manage day-to-day operational processes. Small business owners will realize proper cash flow management is essential.

Profit and cash flow are two financial concepts that help a business make actionable and informed decisions. The more you stay on top of the books, the easier it is to predict cash flow challenges. A profitable business is one that not only realizes the overall profit but successfully manages cash flow.