Marginal cost is a microeconomics concept that businesses adopt to determine cost-effective production or service levels in the short run. In inflationary times, monitoring marginal costs in your company and devising strategies becomes even more vital.

What is Marginal Cost?

Marginal cost is the incremental cost when one additional unit of a product or service is produced, computed as change in total costs divided by change in quantity. A company can optimally increase units of production to the point where marginal cost equals marginal revenue. If marginal revenue is below marginal cost, then the company isn’t making a profit on the extra unit.

Understanding Marginal Cost in Business

Businesses use the economics and cost accounting concept of marginal cost to determine their ideal level of production in manufacturing and service industries.

Marginal cost includes both variable costs and fixed costs of production. Fixed costs remain constant over a relevant range of total production, but increase in steps as additional investments are required to produce more products or services. Variable costs change directly in relation to the volume of production or activity. Parts cost inflation results in higher variable costs per unit.

In manufacturing companies, as certain levels of production are reached, additional fixed costs, from adding production equipment or additional lease expenses for facilities expansion, may be required. Depreciation expense for that equipment and these additional rent or lease expenses are fixed costs that will increase the marginal cost of producing the next unit.

In combination with marginal cost analysis, businesses use variable and fixed costs for different types of financial analysis, trend monitoring, pricing, and decision-making.

Companies compute and monitor trends in their variable expense ratio, which is the ratio of variable expenses to net sales. They compute their contribution margin as sales revenue minus variable costs and use it for product pricing decisions. Break even point analysis provides a clear picture of when the company covers its variable and fixed costs through revenue generation.

Product pricing decisions are analyzed for discontinuing an unprofitable product line, introducing an additional product, and selling products to a specific customer with below-standard pricing.

How to Calculate Marginal Cost

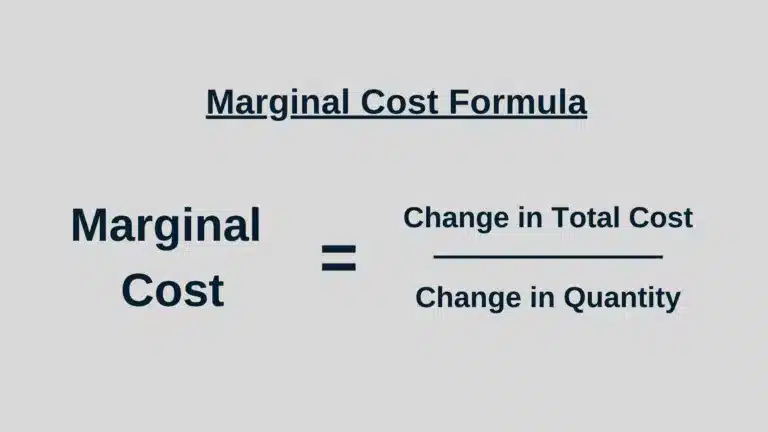

Calculate marginal cost using the marginal cost formula, which measures the cost of producing one additional unit of goods or services provided to a customer.

Marginal Cost = Change in Total Cost

Change in Quantity

Example of Marginal Cost

The per-unit cost of a manufacturer producing 100 sofas is $500, which is a total cost of $50,000. The cost of producing the next sofa rises to $510, with total costs of $50,510 for 101 sofas. Therefore, the marginal cost for producing one additional unit is $510, as calculated below.

Marginal Cost = $50,510 – $50,000 = $510 = $510

101 – 100 units 1

What is Marginal Cost Pricing?

Marginal cost pricing is an ad-hoc strategy to accept orders below the typical selling price per unit. It’s used when a business has excess capacity in manufacturing or another justification. In this case, the variable cost or variable cost plus a small profit may be used to sell extra units that could be produced to a different customer desiring to pay less than the full price of a product.

Marginal cost pricing is used to make some incremental sales with below-normal pricing.

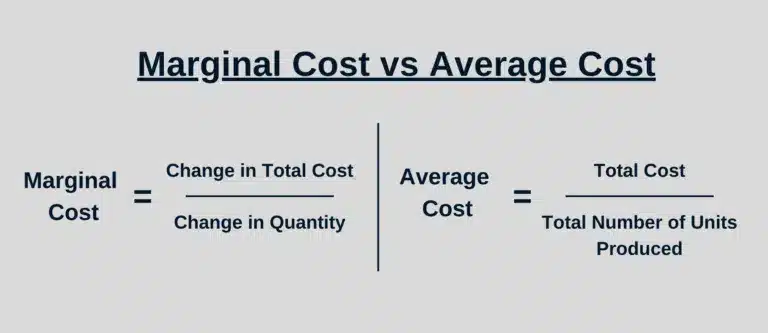

Marginal Cost vs Average Cost

Marginal cost is the addition to the total cost for producing one additional unit. Average cost is the total cost divided by the total number of units produced. When average cost increases, marginal cost is greater than average cost. When average cost decreases, marginal cost is less than average cost. If marginal cost stays the same, it equals average cost.

Economists depict a u-shaped marginal cost curve on a graph that compares it to the cost curve for average cost. The y-axis is average or marginal cost. The x-axis is units of output. These cost curves intersect on the graph. A marginal cost vs average cost graph may show separate curves for the average total cost (ATC) and average variable cost (AVC) in comparison to marginal cost (MC).

Economists depict a u-shaped marginal cost (MC) curve on a graph that compares it to the cost curve for average cost. The y-axis is average or marginal cost. The x-axis is units of output. These cost curves intersect on the graph. When average cost increases, marginal cost is greater than average cost. When average cost decreases, marginal cost is less than average cost. If marginal cost stays the same, it equals average cost.

In accounting, as production increases, fixed expenses in overhead are absorbed (spread) over more units of output, providing economies of scale and resulting in a lower average fixed cost per unit. But the marginal cost may or may not change due to fixed costs. Marginal cost depends on whether investments for production expansion with fixed additional costs are needed, in addition to changes in variable costs.

The Importance of Marginal Cost

Marginal cost is important because businesses can determine their optimum production level for making a profit before costs will increase and monitor increases in variable costs. Marginal cost can be compared to marginal revenue to determine profitability.

Inflation hits a company’s variable costs of producing a product or providing a service and its fixed costs. When anticipating cost changes, the business can create marginal cost and marginal revenue strategies to prepare and react to these cost increases.

For example, a cereal maker in the food industry may shrink its box size or number of ounces to save costs and keep current product pricing.

As another example, a manufacturer with pricing power may increase its prices to offset marginal cost increases with increased marginal revenue. This generates either the same profit level or a spike in profit if they raise prices higher than the inflation rate increases.

Inflation may result in decreasing a company’s total revenues. A company may need to reduce its production volume, raw material purchases, and production or service employees. And a business downturn from a recession would delay the need for additional fixed costs for manufacturing expansion. But it’s a good time for cost control and cost-cutting.

Manufacturers use manufacturing ERP software. They change the master production schedule and revise their purchase order timing with vendors when they need to react to new economic conditions and related customer order changes.

Marginal Cost in Accounts Payable

You can apply the marginal cost concept to accounts payable processing in your business. Your business has a variable cost per invoice and payment and certain fixed costs for processing accounts payable and making payments. Without AP automation software, as the volume of your business grows, you’ll incur additional fixed costs at increasing volume steps for hiring many more accounts payable employees to complete these tasks.

AP automation software will streamline workflow, help your company take early payment discounts, and reduce fraud risk and duplicate payment errors when making global payments. This significantly increases efficiency, cuts costs, reduces the need for hiring, and speeds up the accounting monthly close so you can focus on strategic finance.

To learn more about how Tipalti AP automation and mass payments software can improve your accounts payable invoice processing and payments, read Tipalti’s The Holy Grail of Accounts Payable white paper.