Research confirms that the majority of cross-border payment management practices are not efficient from both a cost and time perspective. Businesses’ current practices often result in reduced productivity, increased labour, expensive payment fees, and hindered relationships with suppliers. However these problems may be solved by applying best practices and software technology to increase cross-border payment effectiveness, including an advanced global payments system.

What are Cross Border Payments?

A cross-border payment is a transaction between banks, financial institutions, businesses, or individuals operating in different countries that may or may not share a border. Cross-border B2B payments are expected to exceed US$40 trillion (CA$55) worldwide by the end of 2024, up from US$37 trillion (CA$51) in 2022, according to a Juniper Research report.

Who Uses Cross-Border Payments?

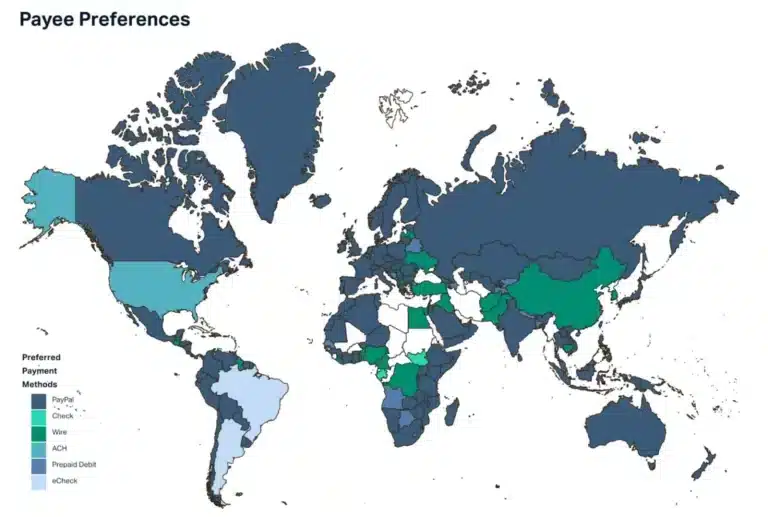

The whole world uses cross-border payments in some form or another. Take a look at Tipalti’s original findings about each country’s preferred cross-border payment method on the map below. Click the map to view its interactive version, where you can see results by payment size range, use the filter, or hover your cursor over a country on the map.

Benefits of Cross-Border Payments

As globalization is increasingly intertwined with the everyday operations of businesses, refining cross-border payment management practices is becoming more important. According to the research, 73% of companies regularly make cross-border payments of some kind. Refining management practices can lead to significant savings and improve international tax and regulatory compliance.

With a solid international payment strategy, businesses can achieve:

- Increased ROI

- Reduced need for resources

- Increased control over international transactions

- Advanced reporting tools

- Enhanced payment security

Interested in making your global payment management practices more efficient? Keep reading to learn how.

Steps to Sending Cross-Border Payments

With cross-border international payments, extra steps and factors must be considered beyond basic steps for domestic payment processing. The following 10 steps for sending cross-border payments include factors unique to cross-border transactions.

1. Purchasing

When sourcing globally, you will find an international supplier you want to purchase from. If you’re buying online through eCommerce, you’ll be directed to the payee’s checkout page to make your B2B payment. If you’re buying over the phone, a sales representative will conduct the checkout process. Either way, you’ll be presented with payment options for your B2B purchase.

Ideally, if you’re buying online, the checkout page will offer a localized experience, meaning it features your native language. The payee uses your URL to determine which language to use for the checkout page and will hopefully offer local payment methods that you are familiar with.

2. Preparing for Cross-Border Payments

Sending a cross-border payment from Canada requires specific information depending on the recipient’s country. It’s important to remember that not all payment options are available in every country. Even if you use Global ACH payments throughout your supply chain, you might need a different method for a new supplier who doesn’t accept it.

Here are some examples of required information for specific countries:

- Within Canada (domestic): Your recipient’s bank name and address, institution number, branch transit number, and account number.

- Cross-border international EFT from Canada: Recipient bank’s ABA (U.S.), SWIFT or BIC code, IBAN, or CLABE (Mexico). Include the reason for the transfer. You can find more information on Payments Canada.

- United States: Your recipient’s bank’s ABA routing number and account number.

- Many European Countries: The recipient’s International Bank Account Number (IBAN).

- Some Countries: A Business Identifier Code (BIC) or SWIFT code.

- Mexico (CLABE)

Ask about early payment discounts when setting up cross-border payments. 40% of companies surveyed in the study mentioned earlier report receiving early payment discounts of 1% to 10% from their suppliers. If you can acquire this kind of discount, you’ll want to use payee prioritization features within your global payments platform to make sure those entities are paid early each month.

3. Verifying Compliance with Global Payment Rules

Verify if you are sending the payment according to all applicable global payment rules. There are more than 26,000 rules, which makes the use of a global payments solution all the more valuable. Can you imagine if your AP department had to check each cross-border payment against that many factors? With a global payments service provider that understands the payments industry, your AP team can focus on core AP tasks rather than on verifying global compliance.

4. Monitoring and Oversight of Global Payments Status

Sending international payments requires maintaining complete oversight of each payment. When making hundreds or thousands of international money transfers, achieving complete oversight can be time-consuming. Using a global payments platform gives you a single platform to view the status of each payment, providing an effective user experience. Instead of checking each payment individually for reconciliation, you can filter them according to ones that are past due or have yet to be reconciled. From there, you can use invoice automation tools to see who is responsible for approving the payment and why it hasn’t been approved.

5. Routing and Processing

Once you enter your payment information, it will be sent via an encrypted gateway to obtain authorization to deduct the funds from your account. Here’s the catch: If you are using a global payments platform that is connected to only one bank, the transaction may be flagged. Using a platform that is connected with multiple banks around the globe improves the chances of the payment being processed the first time around.

Whether you’re paying publishers or setting up a new supply chain, you want to ensure each payment goes through without error. A global payments platform can automate the payment process for you, regardless if it’s a one-time or recurring transaction.

If you are going to make payments to an entity on a regular basis, setting up recurring payments is an excellent way to negotiate pricing discounts. It also ensures the payee is paid on time, which is crucial to maintaining a good relationship.

6. Payment Approval or Denial

Your payment will be approved or declined. Verification takes place to ensure you have sufficient funds in your account, and if necessary, a currency conversion will take place at the current exchange rate. This applies only if you are sending funds in a currency different from the recipient’s account currency.

Hopefully, the cross-border payment is using banks that support international trade by using international payments. If so, the transaction is more likely to be approved. A global payments platform excels in intelligently routing the payment through a bank that is most likely to approve the transaction.

7 & 8. Confirmation (Approval or Denial) and Fulfillment

You will receive confirmation that the transaction has been approved or declined. If declined, you’ll receive a return code outlining why it wasn’t processed. If approved, your order then goes into fulfillment.

9. Settlement

At this point, depending on the type of cross-border payment you’ve used, there’s a good chance the funds will still appear in your account and not in the payee’s. A Global Automated Clearing House (ACH) payment takes anywhere from two to five days to reconcile.

10. Tracking

You will receive a reconciliation report from each bank that you work with. This can be extremely confusing and is an inefficient way to keep track of your cross-border payments. With a global payments platform, you can receive a consolidated reconciliation report showing all payouts through all banks and which transactions have been reconciled, as well as which ones have not.

Struggling with fast and budget-friendly cross-border payments?

Ensuring timely and cost-effective transactions across borders can be a challenge. Don’t navigate the international payment landscape alone – explore automated mass payments and unlock a world of game-changing solutions.

Additional Cross-Border Payment Recommendations

Anna Barnett of PayStream Advisors served as the lead analyst on the research study mentioned earlier. She says that, in order to perform cross-border payments correctly, businesses must have their AP department integrate multiple extra steps and controls into their cross-border payment management strategy.

Validate the Accuracy of Payment Data

An example of an extra step would be to implement a practice that validates the accuracy of payment data. With more than 26,000 global payment rules impacting cross-border payments, using a global payment platform that checks payments against these rules is of the utmost importance.

Use a Single Global Payments Platform

Anna goes on to discuss how international payments are often made via multiple payment rails, making them much more complex than domestic-only reconciliation. Having a single platform to work from streamlines the global payable process.

Integrate Cross-Border Payments into AP Practices

Any business that wants to sell or acquire products and services on a global basis should integrate cross-border payments into its AP practices. Not every payment gateway can process international payments, making it crucial to use one that can. Moreover, using someone who has extensive knowledge of navigating the cross-border payment ecosystem can help make your operations as efficient as possible.

5 Types of Cross-Border Payments

There are multiple global payment methods to choose from. When making payments to overseas affiliates, the supplier chooses a preferred method and then you are responsible for paying according to that method. This is why you should use a global payment platform that supports multiple payment options. More importantly, choose one that allows you to make multiple payments simultaneously, even when they are in different formats and currencies.

1. International Wire Transfers

An international wire transfer offers a fast transfer of funds but typically comes with a wire transfer fee of CAD $30-$50. For smaller transfers (e.g., CAD $500), a CAD $30 fee can be significant. For larger transfers (e.g., CAD $20,000), the fee might be less impactful.

Due to their high cost per transaction, wire transfers are not ideal for frequent or high-volume payments. They also offer limited tracking capabilities. Since routing rules can vary by country, wire transfers may not be the most efficient option for regular B2B transactions.

2. International ACH

Commonly referred to as a Global ACH, an international ACH makes it simple to make payments to overseas suppliers and affiliates. Global ACH payments can be made through various entities, including SEPA, BACS, and local banks, but are not carried out via a card network. They are inexpensive and extremely convenient. The downside to Global ACH payments is that they can take several days to process. Due to their low transaction fees, they are ideal for making large volumes of payment and are very simple to set up on a recurring basis.

You must have the payee’s International Bank Account Number (IBAN) and other account information to make a Global ACH payment. Keeping up with each payee’s account information can be overwhelming without a global payment platform.

3. Prepaid Debit Cards

Also known as cash cards, prepaid debit cards make it simple to pay international affiliates. Your funds are automatically deducted from your account and transferred to the payee’s debit card account. Prepaid debit cards are processed over a card network and provide real-time payments immediacy, which is of immense value when you need to make a quick payment to a global supplier. The transactions often come with a fee for both the payer and payee.

To withdraw funds from the prepaid debit card, the payee will likely have to pay an ATM fee, and there is a confusing reconciliation process. Most importantly, the transactions are not covered by federal consumer protection laws. They are, however, beneficial for making payments to global affiliates who operate in a country with limited banking infrastructure.

4. PayPal

There are two main drawbacks to making global PayPal payments: They come with a high transaction fee, and there is no clear policy outlining how funds are held. You may have one payment clear instantly, while another one to the same entity takes multiple days. PayPal payments between the sender’s and recipient’s digital wallets may require a later transfer by the recipient to a local bank account. Using a global payment platform that supports mass payments with PayPal is an effective way to enhance the payment experience and reduce the workload of up to 80% for the PayPal and other payment payment methods in payables.

5. Paper Checks

When a global affiliate is unable or unwilling to provide bank routing information, you can use a paper check to make an international money transfer. All you need is the payee’s name and an address to mail the check. This type of payment method doesn’t always come with a transaction fee depending on the financial institutions, including any intermediary banks or correspondent banks involved, making it extremely economical. However, it may be weeks before the check is received through postal mail and cashed, which can negatively impact your cash flow management. Paper checks are also prone to fraudulent activity.

How to Save Money with Cross-Border Payments

Your business can save money by making cross-border payments that aren’t through banks. A global payables platform with AP automation software provides added functionality like fraud and error controls and tax and global regulatory compliance. This type of global payment platform yields cost and efficiency benefits beyond lower cross-border transaction costs.

Cross-Border Transaction Costs

The World Bank published the Remittance Prices Worldwide report in December 2023 found that the average cost of sending US $200 (approximately CA$274) remained around 6.4% in the fourth quarter of 2023, which is more than double the Sustainable Development Goal target of 3%. Banks are the most expensive channel for sending remittances, with an average cost of 11.99%, followed by post offices (7.72%), money transfer operators (5.47%), and mobile operators (4.35%).

Global Payables Platform Financial Advantages

As you can see, initiatives such as partnering with a global payables platform can save money on cross-border payments. Reduced transaction fees, however, aren’t the only financial advantage of this type of service provider. When you have a platform automating invoices and global payments, you can reduce AP headcount or redirect those employees toward other pertinent operational tasks.

The invoice automation benefit provided by a cross-border payments platform also reduces overhead expenses and leads to money-saving opportunities by streamlining the end-to-end AP workflow. Manual activities that are normally handled by the AP team can be automated, turning them into “touchless” tasks. The automation software does the heavy lifting for you using intelligent technology to verify and route each invoice correctly. It also pinpoints potential issues and mitigates human error. Faster invoice processing gives you a better view of where early discount pricing opportunities exist, and it serves as a solid foundation for scaling your AP processes.

The built-in optical character recognition (OCR) scanning feature, which is available through invoice automation software, identifies pertinent payee information and records it for future use. Override changes are intelligently identified and then applied to future invoices. After OCR scanning takes place, a second layer of verification is performed to maintain optimal data extraction accuracy. With greater accuracy comes improved invoice processing and reconciliation, which saves money and reduces the AP workload.

A global payments platform also saves money on cross-border payments by allowing you to send money internationally using various payment methods other than a wire transfer. This is of tremendous value when sending payments to countries where wire transfers are not supported. If preferred, you can set payments so that the payee absorbs the transaction fees. Since a global payments platform offers reduced fees, a payee is more likely to absorb them, especially when you point out that you’re sending payments via a method that doesn’t require a wire transfer.

Corporate Benefits of Cross-Border Payments

If you’re looking for ways that international payments can benefit your company, you won’t have to look far.

1. Make Mobile Device Invoice Payments Anytime

Whether you’re an established corporation or a small start-up, globalization will impact your bottom line. With cross-border payments, you can pay suppliers from your smartphone and other mobile devices. This means that, even when you’re away from the office, you can pay an invoice.

2. Automate Intelligent Payment Scheduling

You can use your global payments platform to intelligently schedule every payment for you, allowing you to focus on your core operational tasks rather than concerning yourself with hundreds or thousands of invoices.

3. Increase the Number of Suppliers and Affiliates

Cross-border payments also increase the number of suppliers and affiliates you can connect with. For example, You recruit an amazing freelancer who can create content for your website at a great price. The freelancer is located in a different country and only accepts payment in his local currency. Without cross-border payments, you won’t be able to secure this relationship. With global payables software, freelancers can go through a simple onboarding process whereby they add their payment information. They can send you invoices each month, and reconciliation will be automatic.

4. Conveniently Use a Self-Service Supplier Portal

Probably the most notable benefit of making cross-border payments is the convenience they provide, especially when using a global payments platform. All payee information is uploaded during the onboarding process and an online portal makes it simple for payees to update their information as necessary.

Tips for Choosing a Global Payments Platform

Choose an automated global payments platform that includes the following:

- Mass payment processing

- Integration with algorithmic banking rules

- Advanced payment configuration options and thresholds

- Automatic global regulatory compliance

Mass Payment Processing

To get the most out of cross-border payments, make sure to choose a global payment platform that supports mass payment processing. You’ll be able to schedule thousands of payments using multiple payment methods. Also, choose one like Tipalti, which supports payments to 200+ countries in 120 different currencies. Imagine being able to partner with any supplier or overseas affiliate and pay them through your payment provider in their local currency. This type of payment processing is at the heart of enterprise scalability.

Integration with Algorithmic Banking Rules

No matter the platform you choose, ensure it integrates the 26,000-plus commercial banking rules when processing payments. This will ensure payments are processed quickly and help you reduce errors.

Advanced Payment Configuration Options and Thresholds

Your global payments platform should feature advanced payment configuration options through which you can split transaction fees between you and the payee. Additionally, payment threshold features can give you the ability to hold payments until a predetermined margin is reached, optimizing your margins on transactions and improving your cash flow.

Automatic Sanctions Screening

A global payments platform can simplify your adherence to Canadian sanctions regulations. Similar to how OFAC compliance works in the US, sanctions screening is essential to avoid penalties and reputational harm. A global payments platform automates this process by checking all payees against relevant Canadian and international sanctions lists, reducing the risk of processing payments to sanctioned entities. This safeguards your business from financial repercussions and reputational damage.

Refining Cross-Border Payment Processes

Cross-border payments are transactions sent from one country and received in a different country. Transfer fees, bank fees, local currency, foreign currency conversion rates, exchange fees, and international credit card fees may apply to cross-border transactions. Electronic cross-border payments or money transfers are between online accounts or bank accounts registered in different countries.

Expensive payment fees, time-consuming tasks, and slow payments are the results of inefficient cross-border payment practices. With a first-class global payables automation platform, businesses can address these issues, leading to enormous savings of time and money.

Globalization has revolutionized business possibilities. An increasing number of enterprises are tapping into overseas suppliers, which has sparked a huge surge in cross-border payments. An independent study spearheaded by PayStream Advisors and commissioned by Tipalti discovered that 73% of companies based in the United States are regularly making cross-border payments. Conducting these payments has fueled an extensive need for tax law compliance, particularly when compared to domestic payments.

Does your business need help with making international payments? Read on to learn how to handle cross-border payments in five easy steps.

1. Determine the Supplier’s Preferred Payment Method

Different suppliers and affiliates prefer different payment methods. Available payment options and time preferences will dictate which method is best for each supplier. According to the Performance Marketing Network Payment Satisfaction Survey, 54.7% of publishers and affiliates want better payment options. Of those surveyed, 81.5% agree that having options in payment methods is important or very important.

Automated Clearing House (ACH) and PayPal payments are often highly favoured when conducting small transactions, as the associated fees don’t chip away at profit margins. When making global payments, wire transfers prove fast and secure, but high transaction fees can make them extremely costly. Still, according to the survey, 12.9% of global affiliates don’t mind absorbing wire transfer fees.

33.9% of global affiliates prefer PayPal payments. 41.9% have a preference for local bank transfers, also known as Global ACH, while 21% would rather receive a wire transfer. 17.2% prefer prepaid debit transactions and 16.1% favour paper check payments.

It’s imperative to identify global suppliers’ preferred payment methods. Each one will have various banking fields to comply with, like SEPA codes. Much of the time, if the supplier has a bank account and can give you its specific routing details, conducting Global ACH payments will prove cost-effective. Some suppliers also use virtual payment cards to manage their employee spending.

2. Identify Which Currency to Send the Payment In

Reevaluating your traditional cross-border payment methods can save money. According to Financial Executives International, “Most businesses are overlooking a simple strategy that could help them reduce the cost of their imported goods by as much as 10 percent or more.” This strategy involves altering cross-border payment methods so that the supplier is paid in their own currency.

Some businesses believe paying in a currency other than the U.S. dollar is going to expose them to risks and hinder their bottom lines. What you need to understand is that paying suppliers in their own currency can save money and in some instances, will open doors to new payment terms.

For example, certain global suppliers don’t have a USD account, meaning that in order to accept payments in USD, their banks have to conduct a foreign exchange conversion, which is generally accompanied with a fee. Being paid in their local currency gives suppliers the ability to mitigate conversion fees and achieve better cash flow management. As a result, they will often offer pricing discounts if you agree to make payments in their local currency.

A Datos Insights (formerly Aite Group) survey noted that 60% of respondents who paid their global suppliers in their local currencies were able to negotiate a discount of up to 2%. Even a 1% discount for a middle-market importer will save USD $15,000 for every USD $1.5 million it pays to a supplier.

11% of survey respondents noted even greater discount opportunities, with suppliers offering a 3% to 5% discount for making international payments in their local currencies. To top it off, another 11% of the respondents said they were able to secure discounts of more than 10%.

3. Team Up With a Global Payables Platform

Teaming up with a global payables platform allows you to make mass global payments in a matter of minutes. You can schedule thousands of payments, acquire support for multiple payment methods, take advantage of built-in global regulatory sanctions list screening, and achieve enterprise-grade financial control over your cross-border payments.

A global payables platform eliminates the need to perform data entry across different bank portals and reduces overhead. Using an API, you can send payments in different currencies to all of your suppliers with the click of a button. Most importantly, you can do it from a centralized location. This gives you a bird’s eye view of all of your global payments, which improves your cash flow management.

4. Understand Global Payment Rules

Numerous regulations govern international payments, and non-compliance can lead to penalties. A global payments platform simplifies navigating these complexities by ensuring you use the correct payee information for every transaction. The platform may also allow your supplier to indicate their preferred payment method, streamlining the process and potentially unlocking discounts.

5. Ensure Payment Is Reconciled in Accounts Payable Automation Software

Using a global payables platform to reconcile all global payments proves effective in terms of both cost and time. You can view real-time integrated reports that take the hassle out of having to stitch together thousands of spreadsheets. Every bank statement can be uploaded to a single location, making it simple to prepare for tax season. Use real-time reports to see which suppliers have been paid and which invoices still need to be reconciled.

Handling cross-border payments correctly is crucial to staying compliant with global remittance rules and tax law. Refining your global payment processes by partnering with a global payables platform can help you pinpoint early payment discount opportunities. Furthermore, the instant reconciliation of global payments will shorten the financial close cycle, improve your cash flow visibility, and reduce potentially fraudulent payouts.

How Automation Improves the Cross-Border Payment Process

Automating cross-border payments saves time and money. It communicates respect for your international affiliates by showing them that you want to pay them quickly, effectively, and in their own currency. Automation with the right services provider also reduces currency conversion fees, which is favourable to suppliers. Namely, you can customize the automation software to create an international payment system that optimizes the entire cross-border payment process.

Cross-border payment automation gives you a single platform to make both domestic and international money transfers. This streamlines the AP workflow and provides better AP transparency. You’ll also be able to view payments in real-time, including those that have been reconciled and those that are still due.

Lastly, using global payments automation through a services provider like Tipalti gives you the ability to leverage a payment system that is built to scale. You don’t have to burden your software team with development or maintenance tasks. You’ll have access to a platform that eliminates financial and compliance risks, reduces payment reconciliation times, improves supplier relationships, and, most importantly, increases the ROI on your AP processes. Download our eBook, “Comparing Top Global Payment Methods”.

Using Tipalti to Optimize Your Cross-Border Payments

Tipalti’s AP automation and mass payments software products let your business or nonprofit organization optimize cross-border payments, making the process efficient and more cost-effective.

Tipalti also offers Multi-FX (which supports 30 currencies) and FX Hedging products for additional foreign exchange capabilities and simplification when making global payments. Multi-FX lets your business make payments for all subsidiaries from a centralized virtual payment account. With Tipalti’s FX Hedging for payables, your company can lock in foreign exchange rates before invoices are due for payment.

Tipalti AP automation is for making global payments to suppliers for accounts payable. Mass payments software is for making global payouts to creators, independent contractors, influencers and streamers, ad networks, and publishers.

Tipalti is an advanced global payments solution, with these capabilities:

- Make global payments in 200+ countries and 120 currencies from the Tipalti platform, using multiple payment methods in the same batch for up to thousands of payments

- Automatically reconcile global payments

- Validate suppliers to reduce fraudulent payments

- Use 26,000+ payment rules to flag and reduce errors

- Automate payment status for payees, provide payment method choices, and view payment history in a self-service Supplier Hub