This guide defines what a W-9 form is and provides a link to a fillable Form W-9 from the IRS website. We describe the required information, who requests and fills out a Form W-9, how to prepare a complete Form W-9 and submit it, and why W-9 forms are important. Requesters use W-9 forms (and W8 forms) to prepare IRS 1099 information returns.

What is a W-9 Form?

A W-9 form is an IRS form used to provide a U.S. person’s contact information (including name on tax return), certification, and Tax Identification Number (TIN) to their payer/requester. The official name of the IRS W-9 form is the Request for Taxpayer Identification Number and Certification form.

Form W-9 is the same for all legal entities, from individuals/sole proprietors to C corporations, S corporations, LLC (limited liability company), partnerships, and trusts. For example, it applies to independent contractors, small businesses, nonprofit organizations, and churches.

Where Do I Get a W-9 Form?

If the requester doesn’t furnish a blank Form 1099, the recipient can complete a downloadable blank paper Form W-9, find a W-9 fillable form on the IRS website, or use software that enables inserting W-9 fillable form data.

W-9 preparers must use the latest IRS Form W-9 available and follow IRS guidance from the instructions at the bottom of a W-9 when completing it.

W-9 Official Form Download

The IRS website has a downloadable, blank, fillable, and printable W-9 form PDF you can use for free to submit your W-9 to a requester.

Sometimes the requester will provide a blank IRS Form W-9 to vendors or other payees to return to the requester after completion, instead of directing them to the IRS website to complete a fillable W-9 form online.

Although not recommended, payees can submit a Form W-9 with handwritten information to their requester. This submission method may require W-9 tax form requesters to perform manual data entry, which could result in delays, errors, and IRS penalties from late or incorrect 1099s.

W-9 Collection

Requesters in a trade or business collect W-9 forms from US persons and W8 forms from other payees that earn gross income. The payers will use Form W-9s collected to submit Form 1099 information returns to the IRS and distribute copies to applicable state tax agencies and the recipients (payees).

It’s best practice to request W-9 (or W8) forms from all 1099-NEC and 1099-MISC payees or suppliers during onboarding, before their first payment is made. This eliminates the need for staff to spend time following up to collect forms near each calendar year-end.

W-9 requesters must prepare and submit 1099 forms only when the payment amount or backup withholding exceeds the IRS threshold for the specific calendar year of payments. For calendar 2026 payments reported on Form 1099-NEC for Nonemployee Compensation and for some items reported on Form 1099-MISC, the threshold increases from $600 to $2,000. In later years, the threshold amount will be indexed for inflation.

W-9 Form Validation

For the 1099 information return process, after W-9 collection, businesses must validate the information on each W-9 form to verify completeness and accuracy, and avoid IRS information return penalties that can reach significant maximum amounts. One essential process is TIN matching with the IRS database, which matches the legal name and taxpayer ID on the W-9 form.

Information Required on a W-9 Form

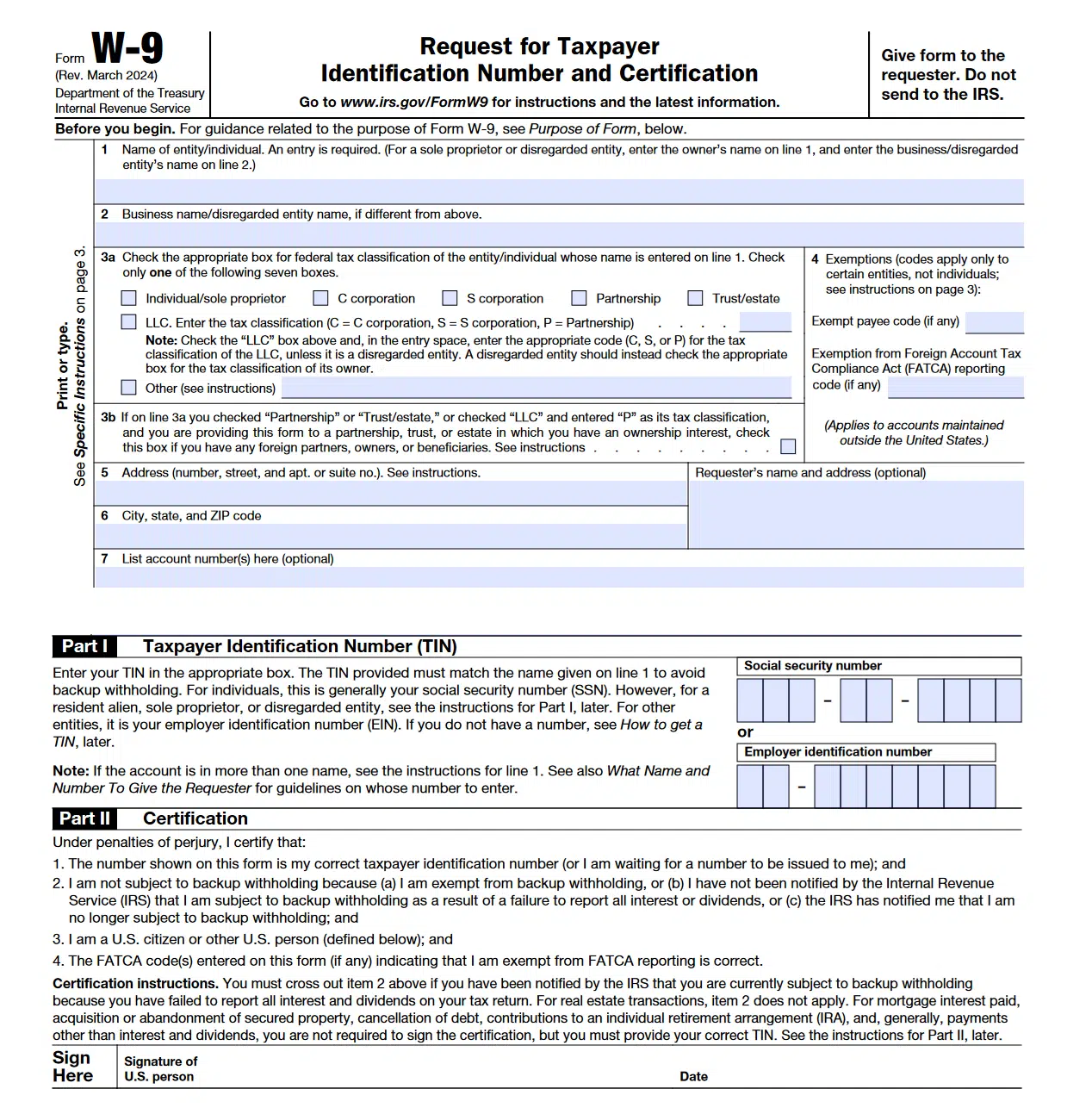

The following information is required on a W-9 form. This sample is a Rev. March 2024 W-9 form that is still being used at the beginning of 2026. Refer to the General Instructions following the form.

Line 1 – Name

Provide the exact name you use on your income tax return.

Individuals who have changed their last name without informing the Social Security Administration should use their first name, last name on their Social Security card, and new last name.

An ITIN is an IRS individual taxpayer identification number. Per form W-9 instructions, ITIN applicants should “enter your individual name as it was entered on your Form W-7 application, line 1a. This should also be the same as the name you entered on the Form 1040 you filed with your Application.”

W-9 tax form instructions for a joint account on line 1 are:

If this Form W-9 is for a joint account (other than an account maintained by a foreign financial institution (FFI)), list first, and then circle, the name of the person or entity whose number you entered in Part I of Form W-9. If you are providing Form W-9 to an FFI to document a joint account, each holder of the account that is a U.S. person must provide a Form W-9.

For “Other entities: Enter your name as shown on required U.S. federal tax documents on line 1. This name should match the name shown on the charter or other legal document creating the entity.”

Line 2 – Business name/disregarded entity name (if different from above)

Besides a business name or disregarded entity name, enter a DBA name or trade name on line 2.

Line 3a – Check one of the seven boxes for federal tax classification (type of legal entity)

The choice of seven boxes includes:

- Individual/sole proprietor

- C Corporation

- S Corporation

- Partnership

- Trust/estate

- Limited Liability Company (LLC)

- Other (see instructions)

For an LLC, in another box to the right of the Limited Liability Company box, enter the tax classification (C=C corporation, S=S corporation, P=Partnership), unless it is a disregarded entity. A disregarded entity should instead check the appropriate box for the tax classification of its owner.

For “Other entities: Enter your name as shown on required U.S. federal tax documents on line 1. This name should match the name shown on the charter or other legal document creating the entity.”

Line 3b – Check this box for certain entities with foreign partners, owners, or beneficiaries

Check this box if you are a partnership (including an LLC classified as a partnership for U.S. federal tax purposes), trust, or estate that has any foreign partners, owners, or beneficiaries, and you are providing this form to a partnership, trust, or estate, in which you have an ownership

interest. You must check the box on line 3b if you receive a Form W-8 (or documentary evidence) from any partner, owner, or beneficiary establishing foreign status or if you receive a Form W-9 from any partner, owner, or beneficiary that has checked the box on line 3b.

Note: A partnership that provides a Form W-9 and checks box 3b may be required to complete Schedules K-2 and K-3 (Form 1065). For more information, see the Partnership Instructions for Schedules K-2 and K-3 (Form 1065).

If you are required to complete line 3b but fail to do so, you may not receive the information necessary to file a correct information return with the IRS or furnish a correct payee statement to your partners or beneficiaries. See, for example, sections 6698, 6722, and 6724 for penalties that may apply.

Line 4 – Exemptions from backup withholding and/or FATCA reporting (codes apply only to certain entities, not individuals)

Exempt payee code (if any): the instructions for Form W-9 provide 13 codes for types of exemptions from backup withholding. For example, Exempt payee code 2 in the Form W-9 General Instructions is “The United States or any of its agencies or instrumentalities”.

Individuals (including sole proprietors) are generally not exempt from backup withholding. Corporations are exempt from certain payments, including dividends and interest, unless they fall under one of the exceptions.

Corporation exceptions requiring backup withholding include “payments made in settlement of payment card or third party network transactions. Also, corporations are not exempt from backup withholding with respect to attorneys’ fees or gross proceeds paid to attorneys, and corporations that provide medical or health care services are not exempt with respect to payments reportable on Form 1099-MISC.”

Exemption from FATCA reporting code (if any)

FATCA reporting applies to accounts maintained outside the U.S. at foreign financial institutions (FFIs). FATCA is the Foreign Account Tax Compliance Act.

If applicable, insert your FATCA code A through M from the W-9 form instructions or indicate “Not Applicable.” You can ask the FFI requesting form W-9 whether a code is required.

Line 5 – Address (number, street, and apt. or suite no.)

Enter your current address and write NEW at the top if it differs from the address you submitted on your W-9 in the payer’s records. You must enter this address to receive your form 1099 information return from the W-9 requester. The payer may still send it to your old address if included in their records. Therefore, the payer should update its records for any change of address (marked NEW).

Line 6 – City, state, and ZIP code

Line 7 – List account number(s) here (optional)

Unnumbered box – Requester’s name and address (optional)

Part I – Taxpayer Identification Number (TIN)

A TIN is a taxpayer identification number used for completing tax returns, W-9 forms, and as identifying information for other purposes, including Social Security, opening bank accounts, and legal transactions.

For Taxpayer Identification, select only one appropriate box from a choice of Social Security Number (SSN) or Employer Identification Number (EIN).

If you are a single-member LLC that is disregarded as an entity separate from its owner, enter the owner’s SSN (or EIN, if the owner has one). If the LLC is classified as a corporation or partnership, enter the entity’s EIN.

If you don’t have a TIN yet, apply for it and write “Applied For” in the space for the TIN. You can get an SSN from the Social Security Administration or an EIN from the IRS. Write “Applied For” if you intend to apply soon for a TIN or have already applied. You have 60 days to receive a TIN for interest, dividends, and tradeable securities transactions payments before backup withholding is deducted.

Individuals usually use their Social Security Number. Individuals may use their EIN or SSN as a sole proprietorship with a registered DBA name (doing business as) or single-member LLC entity name for a small business. A resident alien not having or eligible for an SSN enters their individual taxpayer identification number (ITIN) in the Social Security Number box.

For an LLC registered as a corporation or partnership, enter the EIN.

Part II – Certifications

You will certify, under penalties of perjury, the four items listed on Form W-9. If you are subject to backup withholding because the IRS let you know you didn’t report all interest or dividends on your tax return, cross out item 2.

- You submitted a correct TIN on the W-9 form or are waiting to receive a TIN.

- You aren’t subject to backup withholding for the listed reasons.

- You are a U.S. citizen or other U.S. person, as defined in the instructions.

- The FATCA codes (if any) are correct to report a FATCA reporting exemption.

The face of the Form W-9 indicates when certification or a certification item isn’t required for Form W-9:

For real estate transactions, item 2 does not apply. For mortgage interest paid, acquisition or abandonment of secured property, cancellation of debt, contributions to an individual retirement arrangement (IRA), and generally, payments other than interest and dividends, you are not required to sign the certification, but you must provide your correct TIN.

The General Instructions for Form W-9 define a U.S. person:

Definition of a U.S. person.

For federal tax purposes, you are considered a U.S. person if you are:

- An individual who is a U.S. citizen or U.S. resident alien;

- A partnership, corporation, company, or association created or organized in the United States or under the laws of the United States;

- An estate (other than a foreign estate); or

- A domestic trust (as defined in Regulations section 301.7701-7).

Sign Here

Insert your signature (as a U.S. person) and the date.

Want More Efficient, Tax-Compliant Global Payouts?

Learn how to design scalable global payout workflows that improve speed, accuracy, and tax compliance as your business grows.

Who Requests a W-9 Form?

The requester of a W-9 form tax document is a payer who makes IRS-specified types of payments. The payer or another entity must file a Form 1099 information return to report certain types of transactions to the IRS.

You can learn more about the W-9 vs. 1099 forms and the main differences between them.

Who Fills Out a W-9 Form?

U.S. citizens and “U.S. person” payees who are self-employed independent contractors, freelancers, attorneys, businesses, vendors, suppliers, nonprofit organizations, partnerships, U.S. trusts, heirs of domestic estates, and holders of accounts in U.S. and foreign financial institutions (FFI) complete W-9 tax forms requested by payers and other requesters.

Nonresident aliens who are not employees and work outside the U.S. must submit Form W-8BEN, W-8BEN-E, Form 8233, or other applicable forms instead of a W-9 form.

How to Submit a W-9 Form

Submit a W-9 form to the requester (that may be the payer) required to file an information return, like a 1099 form, to the IRS. Do not submit the completed form to the IRS. You can submit a signed Form W-9 either electronically or on paper.

You may submit a W-9 form as a PDF to the requester or complete a fillable W-9 online using software, complete the Certifications, and sign with an electronic signature.

When Do You Need to Update a W-9 Form?

Besides updating a W-9 for a change in legal name, TIN, or contact information, you need to report a change in your exempt payee status. The Form W-9 instructions include examples of exempt payee status changes, such as a C corporation electing to be an S corporation, or a payee no longer being tax-exempt.

According to the IRS General Instructions following the Form W-9:

You must provide updated information to any person to whom you claimed to be an exempt payee if you are no longer an exempt payee and anticipate receiving reportable payments in the future from this person.

What Types of Information Returns are Prepared From Form W-9?

What is a W-9 used for? Payers of U.S. persons through a trade or business use W-9 forms to prepare different 1099 forms for submission to the IRS and applicable state taxing agencies. The W-9 form requester also provides copies to recipients, who use them to prepare their income tax returns. The taxing authorities, such as the IRS, compare the taxable income on the 1099 form to the recipient’s tax return.

Form W-9 requesters prepare different types of IRS 1099 forms, including Miscellaneous Income Form 1099-MISC and 1099-NEC for Nonemployee Compensation, 1099-INT for interest earned or paid, 1099-DIV for dividend payments, Form 1099-B for stock and mutual fund sales, other broker transactions, and barter exchange.

Other types of 1099s are used as information returns for proceeds from real estate transactions (1099-S), canceled debt (1099-C), merchant card and third-party network transactions (1099-K), and acquisition or abandonment of secured property (1099-A). W-9 forms are also used for Form 1098 for mortgage interest, 1098-E for student loan interest, and 1098-T for tuition.

Importance of Timely and Accurate W-9 Forms

It’s important to provide timely and accurate W-9 forms to requesters. W-9 form payers completing 1099 information returns and W-9 preparers can avoid:

- IRS penalties for inaccurate TIN numbers and information return filing delays

- IRS-triggered backup withholding requirements for inaccurate taxpayer ID numbers

- Unnecessarily withholding taxes from payments to exempt payees

- Delays in information returns, due to the follow-up time staff need to collect missing W-9 forms from payees

It’s best practice to request W-9 forms from all payees during onboarding, such as suppliers or royalty payment recipients, before making their first payment.

The W-9 to 1099 process is:

- Payees submit W-9 forms to trade or business requesters who pay them in the course of business.

- Payers/requesters receive a submitted Form W-9 with each payee’s correct Taxpayer Identification Number (TIN) and other required information.

- The requester prepares 1099 forms for each required payee with total payments at least equal to the IRS threshold amount for the calendar year.

- The requester submits a copy of each 1099-MISC or 1099-NEC form to the IRS and to the applicable states with income tax requirements.

- The payee receives a copy to prepare their federal income tax return for the tax year (and a state copy, when necessary).

- IRS and state tax authorities compare 1099 income and backup withholding status to the amounts reported on the taxpayer’s income tax return.

TIN Matching

Filers of 1099 information return forms prepared from W-9s can use the TIN Matching service available through the IRS website.

TIN Matching compares each Taxpayer Identification Number and name combination to validate. It provides more accurate information to the Internal Revenue Service. If 1099 filers don’t misuse the TINs reported and use TIN matching to avoid an incorrect TIN, they won’t receive as many backup withholding and penalty notices.

IRS Penalties and Backup Withholding Specifics

When the payee provides a correct TIN and certifications on a W-9 form and reports taxable interest and dividends on their tax return, they will not be subject to backup withholding. Backup withholding of U.S. federal income taxes is a 24% deduction from their payment received. The W-9 form submitter will avoid penalties by submitting a correct TIN and accurate information for backup withholding.

Penalties for Businesses as 1099 Preparers Using W-9 Forms

The IRS publishes its Information Return Penalties, which are updated each year for the information return due date. For 1099s and other information returns, the IRS imposes penalties for each incorrect or late information return and payee statement.

As the IRS General Instructions for Certain Information Returns (Section O – Penalties) explains, the maximum penalties for both large and small businesses are substantial. The IRS charges interest on these penalties due, making the potential financial impact on your business even higher.

Penalties For Each Information Return and Payee Statement

| Information Return Due in 2026 | Up to 30 Days Late | Up to 30 Days Late | After August 1 or Not Filed | Intentional Disregard |

|---|---|---|---|---|

| Per each information return and payee statement | $ 60 | $130 | $340 | $680(no maximum penalty) |

| Maximum large business penalty | $683,000 per year | $2,049,000 per year | $4,098,500 per year | |

| Maximum small business penalty | $239,000 per year | $683,000 per year | $1,366,000 per year |

In these General Instructions for Certain Information Returns, the IRS includes some general exceptions to the failure-to-file penalties and defines the criteria for small business information return penalties, as follows.

You are a small business if your average annual gross receipts for the 3 most recent tax years (or for the period you were in existence, if shorter) ending before the calendar year in which the information returns were due are $5 million or less.

W-9 Preparer Penalties and TIN Misuse by Requesters

The Form W-9 General Instructions describe penalties for W-9 preparers and requester misuse of TINs:

Failure to furnish TIN. If you fail to furnish your correct TIN to a requester, you are subject to a penalty of $50 for each such failure unless your failure is due to reasonable cause and not to willful neglect.

Civil penalty for false information with respect to withholding. If you make a false statement with no reasonable basis that results in no backup withholding, you are subject to a $500 penalty.

Criminal penalty for falsifying information. Willfully falsifying certifications or affirmations may subject you to criminal penalties including fines and/or imprisonment. Misuse of TINs. If the requester discloses or uses TINs in violation of federal law, the requester may be subject to civil and criminal penalties.

Misuse of TINs. If the requester discloses or uses TINs in violation of federal law, the requester may be subject to civil and criminal penalties.

W-9 Form Automation

Tipalti customers use Tipalti’s Mass Payments, an add-on cloud software solution that integrates with and syncs with your ERP system to automate global payouts and automatically reconciles payment batches. Tipalti Mass Payments (and Tipalti AP Automation) simplifies W-9 and 1099 workflows.

Tipalti Mass Payments enables making global mass payouts in batches of up to thousands to your independent contractors and creators, including ad network, affiliate, influencer, and royalty payments.

Some requesters prefer that payees submit online digital information for W-9 form automation through their system, rather than using a free W-9 form that the W-9 payees have already completed. Tipalti’s Supplier Hub (payee portal) guides payees for mass payments (or suppliers) through onboarding, which includes submitting their W-9 (or W-8) form information online, providing contact information, and selecting a preferred payment method.

In addition to its other payables and payments functionality, Tipalti Mass Payments automatically handles automated tax compliance, including W-9/W-8 collection, TIN matching for validation, and FATCA compliance. Tipalti will track payments and generate simple preparation reports for 1099-MISC, 1099-NEC, and 1042-S information returns.

Tipalti natively integrates with partnered Zenwork Tax1099 software, which your company can optionally use with a Zenwork SaaS subscription and its per-1099 fees for e-Filing 1099-MISC, 1099-NEC, and 1042-S forms.

Using Tipalti finance automation software, with its KPMG-approved tax engine and AI agents, helps your business meet its 1099 and 1042-S filing deadlines and reduce fraud risks and errors to avoid IRS penalties.

In addition to its tax compliance features comparable to Tipalti Mass Payments, with Tipalti AP automation, your company efficiently processes invoices, enabling it to pay suppliers on time and take any lucrative early-payment discounts the suppliers offer as invoice terms.

Tipalti customers use Tipalti AP automation or Tipalti Mass Payments automation solutions. Tipalti customers may use both software products for making accounts payable invoice payments vs. payouts to independent contractors and creators, such as royalty payments.

Tipalti’s Zenwork Tax1099 Integration

Tipalti natively integrates with partnered Zenwork Tax1099 eFiling software. Users buy a Tax1099 SaaS subscription from Zenwork and pay based on tiered pricing for their 1099 form volume.

Payers using Tax1099 software import 12 calendar months of their Tipalti payments data for suppliers and payees. This payment data is used to generate automatically and eFile information return Forms 1099-NEC and 1099-MISC forms with the IRS and applicable states. Tax1099 also distributes copies to recipients (payees).

Strengthening W-9 Compliance at Scale

Understanding what an IRS W-9 Form is, how to properly fill it out, and how to avoid penalties is important when tracking and reporting payments to your company’s suppliers on a 1099. AP automation software helps you achieve these goals.

Tipalti helps you do the right [vendor] background checks, making sure thereʼs no issue with the bank accounts, and helps collect the necessary tax information, which is really beneficial when doing 1099s at the end of the year.

Becca Simmons, Head of Finance, EMEA, Vivino

Strong W-9 compliance is a critical foundation for accurate 1099 reporting and long-term tax compliance. By standardizing tax data collection and automating validation upfront, businesses can reduce risk, avoid penalties, and confidently scale supplier and partner payments.

With the right automation in place, finance teams can turn W-9 compliance from a year-end scramble into a streamlined, ongoing process that supports growth and audit readiness.

To improve global tax compliance, explore Tipalti’s automated tax compliance solutions.

W-9 Form FAQs

Some frequently asked questions (FAQs) about Form 1099 follow.

What is the purpose of the W-9 form?

The purpose of the W-9 form is to provide information to trade or business payers to prepare 1099 information returns and submit them to the IRS (and applicable states). The 1099 preparer also provides the necessary copies to each payee (recipient) meeting the 1099 threshold for payments (or backup withholding).

The IRS and states use 1099-MISC and 1099-NEC information to verify that the correct income is reported on a taxpayer’s income tax return.

Where can I download the official W-9 form (for 2026)?

You can complete and download the free official fillable W-9 form from the IRS website through this link.

Is there a free printable W-9 form available?

Yes, a free printable W-9 form is available on the IRS website. The requester may provide a printable W-9 form to payees instead.

As an alternative, you may be able to submit your W-9 information by entering it into a secure payee/supplier portal available as part of your Mass Payments or AP Automation software.

How do I complete a W-9 form as an individual or business?

Filling out a W-9 form includes the required information, Certification, and a dated signature. After completion, submit the W-9 form to the requesting business.

Why would a company ask me to fill out a W-9?

A company from which you receive payments would ask you to fill out an IRS Form W-9 to enable it to prepare its 1099 information return forms. 1099s from the payer company are required by the IRS and your state (if it assesses income taxes), and your payments exceed the calendar-year IRS threshold.

Why am I getting a W-9 form?

Payees get or access a W-9 form online to complete and sign. A W-9 form is requested by payers engaged in a trade or business from which they earn taxable income, as described in 1099-MISC and 1099-NEC form Instructions.

Who gets a 1099 form?

Regarding who gets a 1099 form, the IRS, applicable states, and payees who submit a W-9 form and are U.S. persons receive a 1099 form from the W-9 requester if they meet the dollar threshold stated in the specific calendar year’s 1099 form instructions for a 1099-includable line item.

Payers use Form W-9 to prepare their 1099s for each payee and furnish copies of applicable 1099 forms to taxing authorities and the recipients by IRS deadlines following the end of each calendar year.

Can you fill out a W-9 by yourself?

Yes. You can fill out a W-9 form by yourself because it requires entering known data, including the legal name on your personal or business tax return, your taxpayer ID number (TIN), such as SSN or EIN, and other information.

You don’t need a paid preparer to complete a W-9 form, but if you’re unsure of the required information or what a W-9 is correctly filled out, you can ask a qualified preparer how to do so.

Do small business owners need to fill out a W-9?

Small business owners, including independent contractors and suppliers, who are U.S. persons or others designated with legal authority to bind an entity, can fill out a W-9 form. Individual sole proprietors and larger businesses also fill out W-9 forms.