What is a SWIFT Payment?

A SWIFT payment is an international bank transfer that uses the SWIFT messaging network to send secure payment instructions between financial institutions.

SWIFT does not move money itself. Instead, it helps banks communicate the details needed to route, verify, and process cross-border payments. The actual transfer of funds happens through banks, correspondent banking relationships, and payment rails.

Businesses often use SWIFT payments to send money to international suppliers, vendors, partners, and contractors when local payment methods are unavailable or when bank-to-bank transfers are required.

What is a SWIFT Code?

How does SWIFT work? When you use SWIFT, you are not sending a money transfer. Instead, it is referred to as a “payment order” between two banks. This is done using a SWIFT code.

When comparing IBAN vs. SWIFT, the ISO defined the IBAN (International Bank Account Number) standard. SWIFT acts as the ISO 13616 registration authority for IBAN and publishes the IBAN registry. SWIFT is the registrar and administers the BIC (Business Identifier Code / Bank Identifier Code) system, which was standardized under ISO 9362. This means it can identify a bank in seconds and send a secure payment quickly.

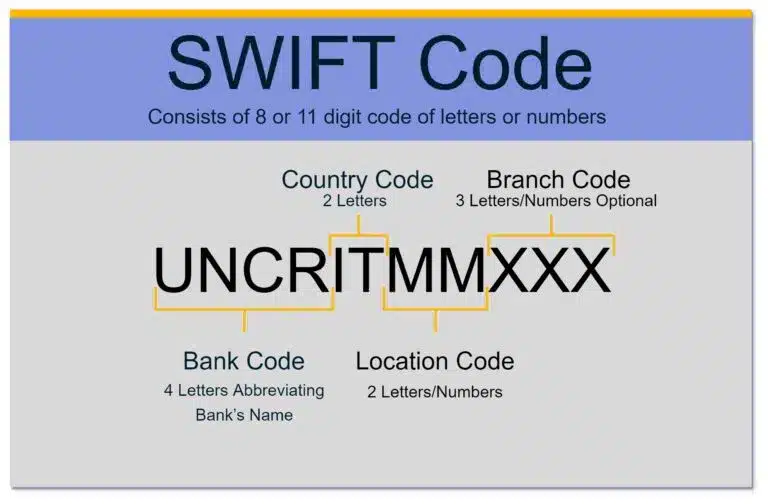

A unique SWIFT code comprises 8 or 11 characters. Other names for this same code include:

- Bank identifier code (BIC)

- SWIFT ID

- ISO9362

Example of a Swift Code

An example of a SWIFT code is that of UniCredit Banca in Milan, Italy. The code is UNICRITMM.

The first four characters (UNCR) are the bank code. The following two characters (IT) are the country code for Italy. The next two characters (MM) represent the bank’s location or city code. The last three characters (which are not shown here) are optional. They are only used by banks to assign codes to individual branches.

Using a SWIFT Code

An example of this in action is when a customer walks into a central bank, such as Bank of America in New York, and wants to make an international money transfer to a friend in Venice through UniCredit Banca. They need their friend’s bank account number and the unique BIC code that applies only to UniCredit Banca and the exact branch in Venice.

Bank of America will then send a SWIFT message to UniCredit Banca over the secure SWIFT network. Once the Italian bank gets the message, it will clear and credit the money to the Italian friend, while Bank of America debits the customer’s account.

Formatting SWIFT Messages

SWIFT messages are formatted using two main standards: the traditional MT (Message Type) format and the modern MX format based on ISO 20022.The MT/ISO 20022 coexistence period for cross-border payment instructions ended on 22 November 2025, with additional data-quality milestones continuing into 2026.

MT messages (such as the commonly used MT103 for cross-border wire payments) rely on a block-based structure with limited data fields. They have been widely used in legacy banking systems.

MX messages utilize XML, providing richer, more structured data that supports greater transparency, automation, and compliance. This makes it ideal for modern financial operations.

As part of a global migration initiative, SWIFT transitioned all cross-border payments to the ISO 20022 (MX) standard in November 2025. This is meant to improve interoperability, accuracy, and end-to-end visibility across all financial networks.

In 2026, SWIFT began rolling out a new retail payments framework for SMEs and consumers to the first 25 banks in June 2026. SWIFT has designed a blockchain-based shared ledger, with limited MVP implementation by banks for live cross-border payments beginning in March 2026.

| Feature | MT Messages | MX Messages (ISO 20022) |

|---|---|---|

| Format | Tag-based and plain text | XML structured |

| First Introduced | 1970 | 2004 |

| Data Richness | Low | High (structured and extended) |

| Standard | SWIFT proprietary | ISO 20022 |

| Migration Status | SWIFT completed its transition to MX | It is becoming a global standard |

| Interoperability | Limited | High (across systems and borders) |

| Use Cases | Traditional banking, legacy | Cross-border, SEPA, real-time |

How Does a SWIFT Payment Work?

The original design and intent of SWIFT were to enable banks to communicate faster and more securely with one another, particularly in processing international payments. The word “communicate” is always used because SWIFT is simply a messenger between banks. SWIFT money does not exist. It conveys the message containing payment instructions from the issuing bank (i.e., the payor) to the remitting bank (i.e., the beneficiary or receiver).

All banks engaged in a SWIFT transfer will move funds from one account to another based on an underlying network of Nostro and Vostro accounts. This refers to accounts that banks have opened up with each other for the sole purpose of executing SWIFT transactions.

Source: researchgate.net

How to Make a SWIFT Transaction

To make a SWIFT transaction, follow these steps:

- Contact your bank: Provide them with the details of the transaction. This includes the recipient’s name, bank name, account number, amount, currency, and any other relevant information.

- Complete the required forms: Your bank will provide you with the necessary forms to initiate the SWIFT transaction. These forms will typically include information on the originator and beneficiary of the transaction, the amount to be transferred, and the currency involved.

- Provide payment: Once the forms are completed, you will need to provide payment. This typically involves transferring the funds from your account to your bank’s account.

- Wait for confirmation: After the transaction has been initiated, please wait for confirmation that the funds have been transferred successfully. This process can take several hours or even days, depending on the number of banks involved and the complexity of the transaction.

SWIFT transactions can be costly, especially for smaller transactions, as they often incur fees from multiple banks. You should also ensure that you provide accurate and complete information to avoid delays or errors in processing.

The Nostro and Vostro Accounts

As both banks maintain a record of money deposited into the account, this results in two mirrored sets of ledgers, known as the Nostro and Vostro accounts.

Nostro refers to the account the bank uses to hold funds, whereas Vostro refers to the account name the bank records in its books.

When both banks have commercial relationships with Nostro and Vostro accounts, SWIFT transfers are direct and immediate. When banks do not have this type of relationship, the SWIFT network must determine the best way to deliver the message. In this case, a third party, or intermediary bank, is required.

You have to find a middleman to handle the transaction. Once a correspondent bank with a commercial relationship to both financial institutions is identified, the SWIFT transaction can proceed. In this case, additional fees will be incurred from the third-party services.

The more intermediary banks involved in the transaction, the higher the cost of sending will be. It will also take longer to send the payment, and there is a higher risk, as more parties are involved.

Automate global payouts with speed, security, and scale

Accelerate SWIFT payments and cross-border transactions with a streamlined, end-to-end global payment solution.

Who Uses SWIFT Payments?

Initially, SWIFT was designed to facilitate communication only about treasury and correspondent transactions. The message format’s design enabled high scalability. SWIFT gradually expanded to provide services for:

- Banks

- Clearing systems

- Money brokers and security broker-dealers

- Corporates

- Non-bank financial institutions

- Treasury market participants

- Asset management companies

- Depositories

- Foreign exchange

- And more…

How Much Does SWIFT Cost?

SWIFT is a cooperative society owned by its members. These members are categorized into classes based on their ownership shares. All members pay a one-time fee, plus annual charges that vary by member class.

Additionally, the messaging system generates revenue by charging users for message types and lengths. These charges will vary based on the bank’s usage volume.

This explains why you pay different fees for international payments from one bank to the next. Another reason is the bank’s commercial policy on international funds transfers.

SWIFT also charges for additional services, including business intelligence, professional applications, global payments innovations, and compliance.

How Does the SWIFT Payment System Work Today?

Currently, SWIFT provides messaging services to over 11,500 financial institutions in 224 countries worldwide, facilitating global business transactions. It uses over 40,000 active payment routes.

In 2026, SWIFT began rolling out a new retail payments framework for SMEs and consumers to the first 25 banks in June 2026. SWIFT has designed a blockchain-based shared ledger, with limited MVP implementation by banks for live cross-border payments beginning in March 2026.

While the network initially focused primarily on simple financial messages and payment instructions, it now sends reference data for a wide range of actions. This includes transactions for:

- Security

- Treasury

- Trade

- System

Economic Sanctions

In the past decade, SWIFT has also been used for economic sanctions. In 2012, the European Union imposed sanctions against Iran, compelling SWIFT to disconnect from sanctioned Iranian banks.

As of Feb. 28, 2022, the United States, the EU, the U.K., and Canada have agreed to levy sanctions against Russia in response to its invasion of Ukraine.

They have decided to remove select Russian banks from the Society for Worldwide Interbank Financial Telecommunication (SWIFT) messaging system.

A Real-World Case Study of SWIFT in Action

UK company AeroTech sources precision parts from global suppliers. They needed to ensure timely, secure payments across different currencies and regions. Delays or errors in payments could disrupt production.

The company partnered with a multinational bank to use SWIFT gpi to execute cross-border payments more efficiently. They chose the “OUR” payment instruction to ensure vendors received full payment without deductions.

Payment Flow

- AeroTech initiated payments using the MT103 message format, entering beneficiary details and the Unique End-to-End Transaction Reference (UETR).

- The SWIFT network routed the transaction through intermediary banks, with each step timestamped and tracked via the Global Payment Initiative (GPI).

- Suppliers received the funds in 1–2 business days, with payment status visible to both AeroTech and the vendor.

Results

- 95% of payments were received within 24 hours, resulting in a 60% reduction in supplier inquiries.

- Real-time tracking improved transparency with overseas vendors.

- Fewer payment errors due to format validation and structured messaging.

SWIFT gpi has transformed our payables process. We now track every cent and know exactly when our vendors are paid — no more black box.

James Liu, CFO, AeroTech Components Ltd.

SWIFT Payments FAQs

What is the SWIFT Payment System?

The SWIFT payment system enables banks and other financial institutions to exchange secure electronic messages about international transactions. It provides a standardized messaging platform that facilitates communication between banks and other financial entities.

What causes delays in SWIFT payments?

Delays in SWIFT payments can be caused by:

• Multiple intermediary banks (each may apply different checks and timelines)

• Manual compliance or AML reviews

• Time zone differences and non-working days

• Currency conversion or FX settlement delays

• Incorrect or incomplete data, requiring manual intervention

Although the SWIFT system has improved speed and transparency, some transactions may still take 2–5 business days to complete.

Are SWIFT payments refundable?

Only under certain circumstances, like:

• When funds haven’t been settled or credited

• If the originating bank sends a cancellation message (camt. 056 for SWIFT MX (ISO 20022) to recall the transfer

• The cancellation must be approved by all banks involved.

Please note that not all cancellations are guaranteed and may incur additional fees.

Are there any fees involved with making a SWIFT payment?

Yes. SWIFT payments generally involve three kinds of fees:

1. Sender bank fees – charged for initiating the transaction.

2. Intermediary bank fees – deducted as payments pass through correspondent banks.

3. Recipient bank fees – may be deducted from the amount before it’s credited.

The payment instructions often determine the fee structure:

• OUR: Sender pays all the fees

• SHA: Sender and beneficiary share the fees

• BEN: Beneficiary pays all the fees (deducted from the transfer)

What happens if a SWIFT payment fails?

SWIFT payments can fail due to a variety of reasons, like:

• Missing or incomplete documentation

• Incorrect details (like account number or the SWIFT/BIC code)

• Compliance or sanctions, such as flagged names or jurisdictions

• Closed or frozen accounts

• Rejection by intermediary or beneficiary banks for formatting issues

To minimize the risk of your SWIFT payment being rejected, always verify the recipient’s details and ensure that all required documents are complete and accurate.

Can I track a SWIFT payment?

Yes, you can track a SWIFT payment. However, your ability to do so depends on the bank and the payment solution.

If your payment was sent using SWIFT GPI (a service offered by most major banks), you get real-time tracking similar to parcel tracking. GPI provides a unique tracking code (UETR: Unique End-to-End Transaction Reference) that enables both the sender and receiver to monitor the progress through the SWIFT network.

If your bank doesn’t support GPI, tracking may be more limited. In this case, your financial institution will initiate a manual payment status check through the SWIFT network. Please note that this process can be time-consuming and often lacks transparency.

The Future of SWIFT

Although there are other real-time messaging services, such as Ripple, Fedwire, and the Clearing House Interbank Payments System (CHIPS), SWIFT maintains a dominant position in capital markets. There’s a good reason for that, too.

The attributed success is due to the network’s continuous addition of new message codes to transmit different kinds of financial transactions. In other words, it constantly adapts to new financial needs and fintech processes. This makes it the most reliable, flexible, and functional system for international wire transfers globally.

If your business is considering using SWIFT as a messaging network, understanding the process is a good first step! However, there are numerous options for paying international suppliers, including prepaid debit cards, international ACH, wire transfers, and more.

Explore our latest eBook: Providing a First Class Global Payouts Experience to help you decide.