While “SWIFT” can also refer to Apple’s programming language, this article focuses on SWIFT, the global financial messaging network used for international bank transfers.

The SWIFT Banking System

SWIFT (Society for Worldwide Interbank Financial Telecommunications) is a global cooperative that functions as a vast international messaging system.

Members (banks and other financial institutions) use it to quickly, accurately, and securely send and receive information, primarily money transfer instructions. Essentially, it is a sophisticated conduit for international electronic funds transfers (EFTs).

Ownership and Governance

SWIFT is a member-owned cooperative headquartered in Belgium and overseen by global central banks and financial regulators, helping ensure the security and reliability of the network.

Understanding SWIFT

SWIFT is not a financial institution, but it provides a messaging system that operates within a member banking system for money transfers, securities, and treasury transactions. It doesn’t move money. Instead, it’s a messaging system that facilitates the transfer of funds between member banks and other member financial institutions.

SWIFT is essentially a payment messaging network that allows individuals and businesses to take electronic or card payments, even if the customer or vendor uses a different bank than the payee. Members pay a one-time joining fee plus annual support charges based on their classification.

The SWIFT messaging network has become a crucial part of the global financial infrastructure that uses SWIFT transfers. According to the SWIFT 2025 Annual Review, in 2025 alone, more than 11,500 global SWIFT member institutions sent an average of 59.8 million messages per day through the network across over 200 countries and territories. That represented a 12% increase over 2024.

While SWIFT retains its dominant position in the processing of global payments, including cross-border payments, it has begun expanding into other areas. Among them are reporting utilities and data for business intelligence. SWIFT extends beyond financial messaging to provide a platform-as-a-financial-system for transaction management services.

How Does SWIFT Work?

SWIFT operates as a financial messaging system by assigning unique BIC codes to international money transfers initiated by its member financial institutions. The SWIFT network is also used for securities transactions and some other purposes. The SWIFTNet messaging platform has four messaging services.

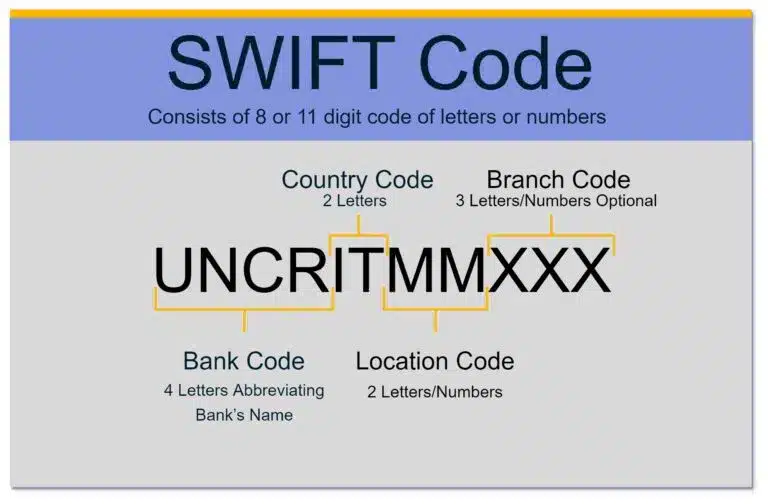

What is SWIFT Code?

SWIFT uses codes to facilitate money exchanges. It assigns each member organization a unique BIC code, either 8 or 11 characters long.

The SWIFT business identifier code is used as a message-system connected BIC to identify the financial institution/bank name with an institute code, the country, bank location city, and, if applicable, a branch code. Additionally, a non-connected BIC refers to its non-financial members. The BIC facilitates accurate transaction routing for bank and other financial institution members.

That code goes by any one of the following names:

- The business identifier code (BIC code)

- Bank identifier code

- SWIFT code

- SWIFT ID or ISO 9362 code

Example of a SWIFT Code

For example, the code for the Italian bank UniCredit Banca based in Milan is UNCRITMM.

- The first four characters comprise the institute code – UNCR for UniCredit Bank

- The next two characters represent the country code – IT for Italy

- Last two are the city where the bank is located – MM for Milan

There is no specific branch code in this case, so the funds will be made available in the Milan headquarters bank.

What is SWIFTNet?

To facilitate transactions, members use a proprietary messaging platform called SWIFTNet. Due to the increasingly complex and diverse requirements of its members, SWIFTNet offers four messaging services that each allow seamless “straight-through” processing:

FIN

FIN is SWIFT’s original messaging service that enables the exchange of messages formatted with SWIFT’s MX (ISO 20022) standards. These are widely accepted and used by the financial community. SWIFT’s FIN can be used for making secure interbank payments and correspondent banking.

InterAct

Like FIN, InterAct enables message-by-message exchanges and supports the exchange of proprietary formats between market infrastructures and their customers. InterAct offers greater flexibility, including store-and-forward, real-time, and query-and-response messaging options. It also enables the exchange of MX message types, developed in accordance with the ISO 20022 standard methodology.

FileAct

FileAct enables the transfer of large batches of messages, such as bulk payment files, very large reports, and operational data.

WebAccess

WebAccess allows SWIFTNet users to browse financial websites securely using standard Internet technologies and protocols.

Customers can connect to the SWIFT environment in different ways:

- Directly via permanent leased lines

- The Internet

- SWIFT’s cloud service (Lite2)

- Directly via their appointed partners

SWIFT offers a range of interfaces that provide seamless links between users’ internal systems and the SWIFT environment. The SWIFT Developer Portal includes over 20 APIs and tools for real-time data exchange.

How Long Does a SWIFT Payment Take?

The time it takes for a SWIFT payment varies by the payment rail used and the destination country, ranging from real-time or same day to 5 days.

Payment rails used for SWIFT payments include:

- Wire transfers

- Real-time payment networks / where based:

- CHAPS (Clearing House Automated Payment System) / UK

- CHATS (Clearing House Automated Transfer System) / Hong Kong

“75% of SWIFT payments reach destination banks within 10 minutes, and many are completed in seconds,” according to the 2025 SWIFT Annual Review. SWIFT is the financial messaging service for payment instructions that facilitates payments made through other payment rails, such as wire transfers.

How Much Does a SWIFT Payment Cost?

SWIFT payment costs consist of international wire transfer sending costs of $35-$65, receiving bank’s $10-$25 fee deduction, each intermediary bank’s fee of $15-$50, a 1-4% currency exchange markup fee, and small SWIFT FIN message and Request for Transfer (RfT) costs per transaction.

Example of SWIFT Transaction

As sophisticated as SWIFT payment technology is, using it is pretty straightforward.

For example, suppose a Bank of America branch customer in New York wants to send money to a friend who banks at the UniCredit Banca branch in Venice, Italy. The New York customer can walk into a Bank of America branch with the friend’s account number and UniCredit Banca’s unique SWIFT code for its Venice branch.

Bank of America will send a payment transfer SWIFT message to the UniCredit Banca branch over the secure SWIFT network. When UniCredit receives the SWIFT message about the incoming payment, it will clear and credit the money to the Italian friend’s account.

It’s as simple as that for the user.

IBAN vs. SWIFT

IBAN and SWIFT codes serve different purposes in international payments. An IBAN (International Bank Account Number) identifies a specific bank account, while a SWIFT code (or BIC) identifies the financial institution involved in the transfer. Together, they help ensure cross-border payments are routed accurately and securely.

Costs are essentially the same for both (bank transfer fees, commissions, exchange rates), and sometimes both codes are required for an international transaction.

IBAN vs. SWIFT vs. Wire Transfer

| Feature | SWIFT | IBAN | Wire Transfer |

|---|---|---|---|

| Purpose | Identifies the financial institution and messaging route | Identifies bank account | Actual electronic transfer of funds |

| Used for | Messaging international payment instructions | International payments | Domestic and international payments |

| Required? | Often | Often in Europe and many countries | Yes, for the transfer itself |

Optimize your global payments with the right method

SWIFT simplifies global payments, but exploring other methods can cut costs, boost efficiency, and streamline transactions.

What Can SWIFT Be Used For?

Today, over 50 years since its inception, SWIFT’s integration and messaging management solutions support a broad range of applications. They range from the complex, high-volume messaging needs of the world’s largest institutions to the lower-volume, cost-sensitive needs of smaller banks (like the one in the example above) and corporate entities.

SWIFT products and services are as varied as the financial industry itself:

- Offers a range of access options

- Produces messaging management software packages

- Carries out macro-economic analyses

- Enables back-office automation

- Supports financial crime compliance and standards implementation

- Offers professional training

- Helps users enhance their security and resilience

In addition, SWIFT connections offer access to many valuable applications, such as real-time instruction matching for treasury and foreign exchange (forex) transactions. Access also extends to securities market infrastructure for processing, clearing, and settlement of payments, securities, forex, and derivatives transactions.

SWIFT introduced dashboards and reporting utilities that give clients a real-time view to monitor messages, activity, trade flow, and export reporting. Users can then filter this information based on region, country, message types, and related parameters.

SWIFT even offers utilities and reporting for “Know Your Customer” (KYC) identity verification, anti-money laundering (AML), and sanctions.

Who Uses SWIFT?

SWIFT founders designed the network to facilitate communications about treasury and correspondent transactions only. The system is so robust that SWIFT has gradually expanded beyond its original mission. It now offers services to:

- Banks

- Corporate businesses

- Foreign exchanges

- Clearing systems

- Asset management companies

- Money brokers

- Non-bank financial institutions

- Depositories

Why is SWIFT Dominant?

While message systems and apps such as Fedwire, Ripple, and Clearing House Interbank Payments System (CHIPS) have evolved, SWIFT continues to rank as the world’s leading financial messaging system.

How? Possibly because it regularly adds new message codes to transmit different financial transactions and enhance the security finance capabilities of its platform.

SWIFT is also expanding its scope. Although it started primarily for simple payment instructions, SWIFT now sends billions of messages each year for actions ranging from security and treasury transactions to trade and system transactions.

The 2025 SWIFT Annual Review showed that only 43.5% of SWIFT traffic is still for payment-based messages, while 51.5% represents security transactions. The remaining traffic flows to treasury, trade, and system transactions.

Brief History of SWIFT

Before SWIFT, Telex was the only way to confirm international wire transfers. Low speed, security finance concerns, and a free message format undermined its effectiveness.

Moreover, it lacked a unified system of codes to identify banks and financial institutions. Telex senders had to describe every transaction in sentences that the receiver then had to interpret. Human error and slower processing times hampered this approach.

In 1973, 239 banks from 15 countries came together to collaborate on a better way to handle communications for international payments. The central banks formed a cooperative utility called the Society for Worldwide Interbank Financial Telecommunication (SWIFT), headquartered in Belgium.

SWIFT went live with its messaging services in 1977, replacing the cumbersome Telex technology. It rapidly became a reliable global partner for institutions worldwide. In 2025, SWIFT spanned every continent, 200+ countries and territories, and provided services to more than 11,500 institutions worldwide.

The main components of the original services included:

- A messaging platform

- A computer system to validate and route messages

- A set of message standards

The standards were developed to:

a) allow for a common understanding of the data across linguistic and systems boundaries; and

b) permit the seamless, automated transmission, receipt, and processing of communications exchanged between users.

Political Influence – SWIFT Sanctions

Because SWIFT is used by institutions worldwide, governments and regulators can require the network to disconnect sanctioned banks. High-profile examples include sanctions affecting certain Iranian and Russian financial institutions.

SWIFT and Global Finance

SWIFT remains a foundational part of global finance because it gives banks, financial institutions, and other participants a standardized way to exchange payment and transaction messages across borders. Its shared messaging standards help reduce ambiguity, support automation, and make it easier for institutions in different countries to communicate using a common financial language.

Although SWIFT does not move money itself, its network helps coordinate many international payments, trade confirmations, securities transactions, and treasury communications. That role makes SWIFT an important part of the infrastructure behind global commerce.

SWIFT Remains the Foundation of Global Financial Messaging

For more than 50 years, SWIFT has served as the trusted messaging network behind international banking, enabling financial institutions to exchange payment instructions securely, accurately, and at massive scale. While SWIFT doesn’t move money itself, its standardized messaging framework helps banks, businesses, and financial institutions coordinate trillions of dollars in cross-border transactions each year.

As global commerce continues to expand, organizations need payment solutions that balance speed, security, cost, and reach. Although SWIFT remains a critical component of international payments, businesses today can also benefit from evaluating alternative payment methods, local payment rails, and multi-rail strategies that may reduce costs and improve payment efficiency for specific use cases.

Whether you’re paying international suppliers, contractors, partners, or customers, understanding how SWIFT works is an important first step toward building a more effective global payment strategy.

To learn more about the payment methods available for cross-border transactions, explore our Global Payment Methods Guide and discover which options best fit your business needs.