Business is evolving, and global commerce is getting easier by the minute. People have a deep desire to collaborate, and we have the financial technology to make it happen.

The SWIFT service sends payment instruction messages to create an international level of connectivity that speeds up global commerce and brings the world a little closer together. It provides a safe and secure means to facilitate cross-border payments and helps banks build an intermediary network.

In 2026, more than 11,500 global SWIFT member institutions sent an average of 53.3 million FIN messages per day across 224 countries and territories.

If you’re looking to streamline international transactions, elevate overseas commerce, and ensure security, the SWIFT network is a prime option.

What is a SWIFT Code?

A SWIFT code is a standard format used for international bank-to-bank transfers. It identifies the branch, bank, and country where an account is registered and communicates the who, what, and where through BIC (Bank Identifier Codes).

SWIFT stands for the Society for Worldwide Interbank Financial Telecommunication. SWIFT is a secure cross-border financial messaging system. It registers and administers the BIC system. It can identify a bank in seconds, to which SWIFT financial institution members send payments quickly using SWIFT messages and a separate entity’s payment rail.

Similarly, ISO defines the IBAN standard, while SWIFT acts as the ISO 13616 registration authority and publishes the registry for IBAN (international bank account numbers)

The SWIFT network uses BIC codes in payment messages for secure payments like international bank wires, international money transfers, and SEPA payments.

When a business uses the SWIFT network, they are not actually sending money. Instead, it is referred to as a “payment order” between two banks.

Other names for a SWIFT code include:

- SWIFT ID

- BIC code

- ISO9362

SWIFT vs IBAN: What’s the Difference?

SWIFT codes and IBANs are often used together in international payments, but they serve different purposes. A SWIFT code identifies the financial institution involved in the transaction, while an IBAN identifies the specific bank account receiving the funds.

| SWIFT/BIC | IBAN |

|---|---|

| Identifies a bank | Identifies a bank account |

| Used globally | Used primarily in Europe and select countries |

| 8–11 characters | Up to 34 characters |

| Required for many international transfers | Required for transfers in IBAN countries |

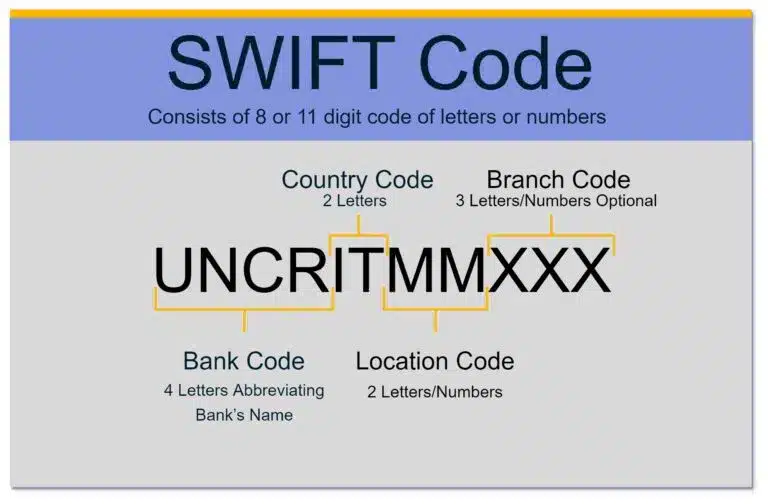

Format of a SWIFT Code

The SWIFT code is an 8-11 alphanumeric character code structured in a standard format from left to right as:

- Bank code (four letters abbreviating the bank’s name)

- Country code (two letters representing the country)

- Location code (two letters or numbers for the bank’s head office)

- Branch code (3 letters or numbers for the bank branch)

The branch code is much like a routing number used in the US. Some SWIFT codes simply use XXX in place of the branch code. In this case, the transfer will go to the bank’s main office.

The International Standard for SWIFT/BIC codes is ISO 9362, which is why you sometimes see this term used in place of SWIFT. The ISO is responsible for the structure of SWIFT codes, including the use of letters and numbers, as well as the length of codes.

Example of a SWIFT Code

One example of a SWIFT code is UniCredit Banca, an Italian bank. It’s located in the city of Milan and has the code:

UNCRITMM (XXX)

- UNCR is the bank code for UniCredit

- IT is the country code for Italy

- MM stands for the location code, which is Milan

As you will see, there is no specific branch code for this bank. Therefore, the transfer will be sent to the primary office in Milan.

When is a SWIFT Code Needed?

A SWIFT code is generally needed when you are sending or receiving money internationally between banks, particularly if you are sending wire transfers or SEPA payments.

Originally, SWIFT was created to facilitate communication about treasury and correspondent transactions. However, the messaging format’s functionality enabled large-scale scalability.

SWIFT now provides services for:

- Banks

- Corporates

- Foreign exchange

- Clearing systems

- Asset management companies

- Money brokers

- Non-bank financial institutions

- Treasury market participants

- Depositories

- And more…

How Does a SWIFT Code Work for International Payments?

The original design of SWIFT was to enable banks to communicate more efficiently and securely among themselves. Particularly in relation to processing international payments.

The word “communicate” is always used because SWIFT is only a messenger between banks. The code basically breaks down payment instructions from the issuing bank (the payor) to the remitting bank (the beneficiary/receiver).

A SWIFT code is used by financial institutions like banks and clearing systems to identify where to send money internationally. This includes the recipient’s bank, the sender’s bank, and the location the funds end up.

In addition to the sending and receiving banks, a SWIFT payment may also require an intermediary bank. Different countries have different banking rules, and sometimes a third party needs to step in to complete the transaction.

For the SWIFT system to fully function, banks open accounts with each other called Nostro and Vostro accounts.

Nostro and Vostro Accounts

Since both banks need to keep records of withdrawals and deposits, this results in two mirrored ledgers: Nostro and Vostro.

Nostro

Nostro is Latin for “ours” and refers to an account a bank holds with another bank in a foreign location.

Vostro

Vostro means “yours,” and it’s how a bank refers to accounts other banks have with them.

When both banks have a relationship through Nostro and Vostro accounts, SWIFT transfers are immediate and direct. When banks do not have this relationship, the SWIFT network must seek the help of a third-party intermediary bank.

Once a correspondent bank is located (meaning they have a relationship with the other two banks involved), the SWIFT transaction can proceed. The more banks involved in these international transactions, the more fees will be incurred. It may also take longer, and there may be more risk involved.

How to Find a SWIFT Code

A SWIFT code can be easily located in a variety of places. Here are a few:

- Bank account statements

- Online banking customer portal

- Bank’s website

- Call the bank

You can also find it online with a quick SWIFT code search tool.

How to Check a SWIFT Code

There are resources online to check and validate a SWIFT code once you have it. Just copy and paste the code into a SWIFT code checker, and the search engine will tell you whether it’s valid or not. Since international banks list these codes online, it doesn’t take long to make sure the one you have is accurate.

The Future of SWIFT

SWIFT continues to retain a dominant position in capital markets despite competition from other real-time message services. There’s a method to that madness.

The network continuously updates its database with new message codes to accommodate a wide rangeall kinds of financial transactions. SWIFT is constantly adapting to fintech processes and changing financial needs.

This makes it one of the most useful and adaptive systems for international transfers worldwide.

Simplify International Payments and SWIFT Code Management

SWIFT codes remain a critical part of global payments, helping financial institutions route payment instructions accurately and securely across borders. While understanding how SWIFT codes work can help businesses avoid delays, failed payments, and unnecessary fees, managing international payment details manually becomes increasingly complex as payment volumes grow.

Modern finance teams need a reliable way to collect, validate, and maintain banking information—including SWIFT/BIC codes, IBANs, and local account details—while ensuring payments reach suppliers worldwide quickly and accurately.

Tipalti helps businesses streamline global supplier payments with automated payee onboarding, banking detail validation, and support for multiple international payment methods across 200+ countries and territories. By reducing manual data entry and payment errors, organizations can improve payment accuracy, strengthen supplier relationships, and scale global operations with confidence.

Explore Tipalti Mass Payments to see how leading businesses automate and scale global payment operations.

SWIFT Code FAQs

When it comes to the topic of SWIFT codes, some common questions that pop up include:

Is a SWIFT Code the Same as a BIC?

BIC stands for Bank Identifier Code, and it’s the umbrella term for a SWIFT code. International bank statements may list them either way. So, keep an eye out for either term if you’re trying to find one.

Does it Cost Money to use a SWIFT Code?

Typically, it costs money to send money internationally, no matter what. Your rates just depend on where it’s going, how it gets there, and who’s involved. Some banks charge fees that they are willing to waive if you have an account.

If you’re sending funds to a bank that requires an intermediary, then there will be additional charges involved that your bank may not be able to avoid. There are also exchange rates to consider.

Additionally, SWIFT offers extra services, such as business intelligence, professional apps, global payments innovations, and compliance.

What Happens if You Give the Wrong SWIFT Code (BIC)?

If you give the wrong SWIFT code, in the best case, it’s rejected by the SWIFT network and the funds are returned in one to three weeks. This is still quite a pain, especially for small businesses.

A minor issue, such as the wrong branch code, can be repaired quickly. However, don’t rely on the banks to fix your mistake.

To avoid delivery problems, use an online SWIFT checker to confirm that the receiving bank’s SWIFT number is correct. It never hurts to double-check.

Is a SWIFT Code or BIC Like a Routing Number?

A SWIFT code is similar to a U.S. routing number used for domestic transactions. However, they differ significantly in structure, subcodes, and function. SWIFT will get your payment overseas. A routing number will not.

Is a SWIFT Code the Same as an IBAN?

The main difference between SWIFT and IBAN lies in what the codes convey. A SWIFT code identifies a specific bank, whereas an IBAN identifies an individual account.

To date, the SWIFT network is the most popular international payment system, surpassing the IBAN (International Bank Account Number) system. The comparison of IBAN vs SWIFT is measured by the number of transactions.